Goldman Sachs says in a latest preview for Wednesday’s key Federal Open Market Committee (FOMC) meeting, “The Fed needs to see substantial further progress on employment and inflation to conclude that tapering is appropriate, which is unlikely to happen until the second half of 2021.”

This report also says that the US central bank may want to give ample warning before the first taper, likely in Q4 2021 or Q1 2022. As per the review “The FOMC’s tolerance for any future tightening in financial conditions might be somewhat greater than usual at a time when activity is picking up and powerful growth impulses from reopening, fiscal stimulus, and pent-up savings are set to support the economy all year.”

US Secretary of State Antony Blinken on Wednesday said that China is acting more aggressively and more repressively, including East China and the South China Sea.

On Tuesday, Blinken said that the US will push back when China uses coercion and aggression to get its way, in his address to the American embassy staff in Tokyo.

On the other hand, in the previous week, a very strong employment report supported the CAD. The headline rate rose 259.2k, topping expectations of 75k, while this was led by the part-time jobs increase, there was also good gains in full-time employment. Meanwhile the unemployment rate fell to 8.2%, significantly below expectations of 9.2%.

Also few days ago the Bank of Canada’s March policy decision came in as expected, with interest rates held steady and asset purchases unchanged. The accompanying statement recognized the resilience of the Canadian economy and stronger than expected economic growth, while also noting that considerable slack and a great deal of uncertainty remains. The BoC Governing Council noted that despite improvements in the economic outlook, “the recovery continues to require extraordinary support.”

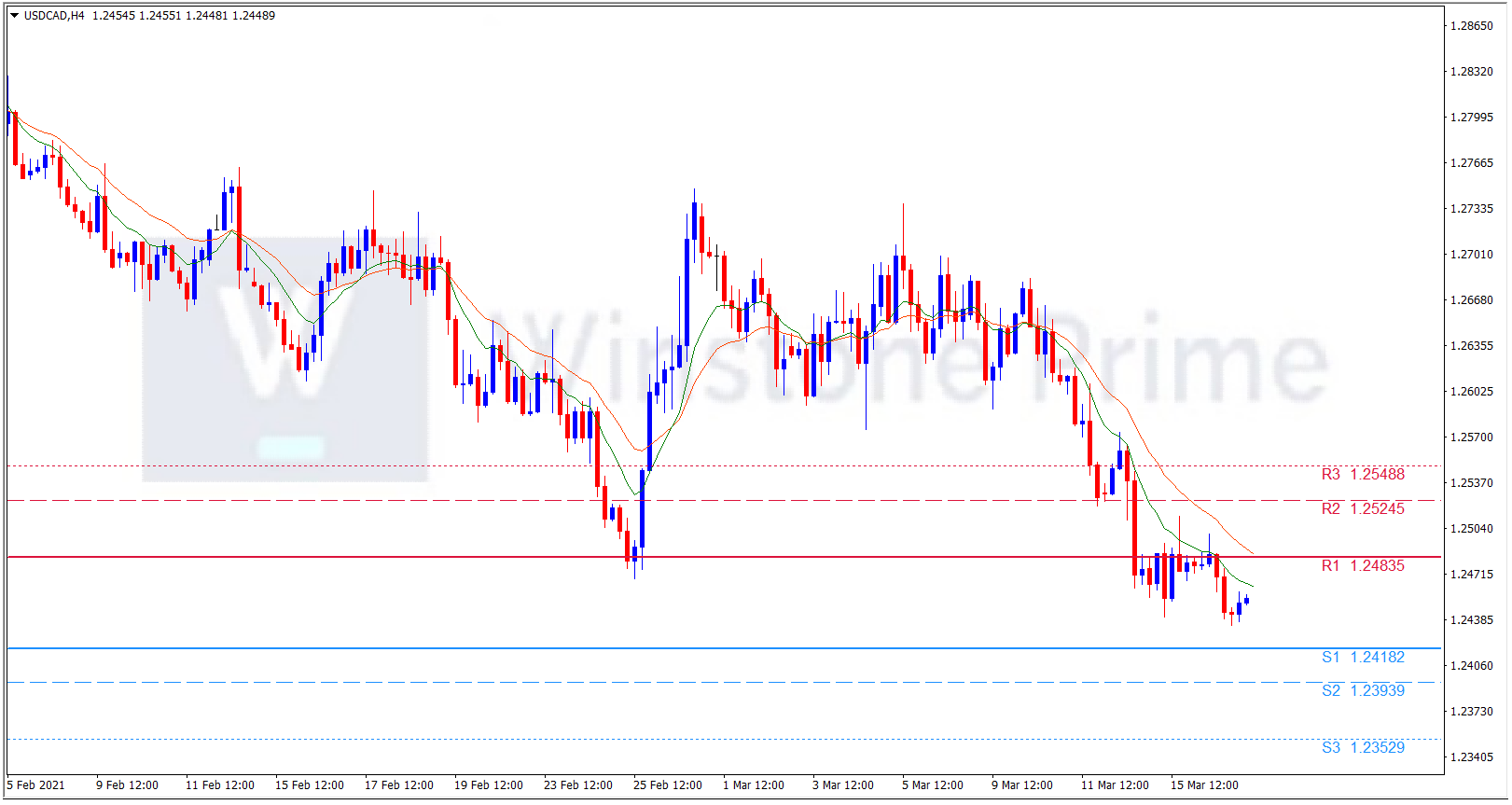

USD/CAD 4 Hour Chart:

Support: 1.2418 (S1), 1.2394 (S2), 1.2353 (S3)

Resistance: 1.2484 (R1), 1.2525 (R2), 1.2549 (R3).

In the prevailing environment which favors the Canadian dollar against the American dollar, we expect a bearish trend for USD/CAD.