Fundamental view:

The Aussie seesawed between bullish and bearish trend to end the week around 0.7760 level. The Australian currency has been stronger in the pandemic if it was not because of China. Tensions between both countries, with the first pressuring to discover the origins of covid and the latter banning imports from the commodity-producer country. It should be noted that Australia suffered as much as any other major economy from the pandemic setback. The number of contagions and deaths is minimal compared to other countries, but at the expense of closing borders for over a year. Just in this week, the country resumed travelling with its neighbour New Zealand.

Reserve Bank of Australia has established an ultra-loose monetary policy that plans to maintain at least until 2024, when policymakers expect employment and inflation to return to more comfortable levels. Which also favored AUD.

US Chicago Fed National Activity Index on 22nd April and US Existing Home Sales on 23rd April created bearish trend for the pair whereas US EIA Heating Oil Stocks Change on 21st April and Australia Commonwealth Bank Manufacturing on 23rd April created bullish trend for the pair.

The major economic events deciding the movement of the pair in the next week are US Core Durable Goods Orders monthly report at April 26, US CB Consumer Confidence Index at April 27, RBA Weighted Median CPI quarterly report, Fed Interest Rate Decision at April 28, US GDP quarterly report at April 29, RBA Private Sector Credit monthly report and US Employment Cost Index at April 30.

AUD/USD Weekly outlook:

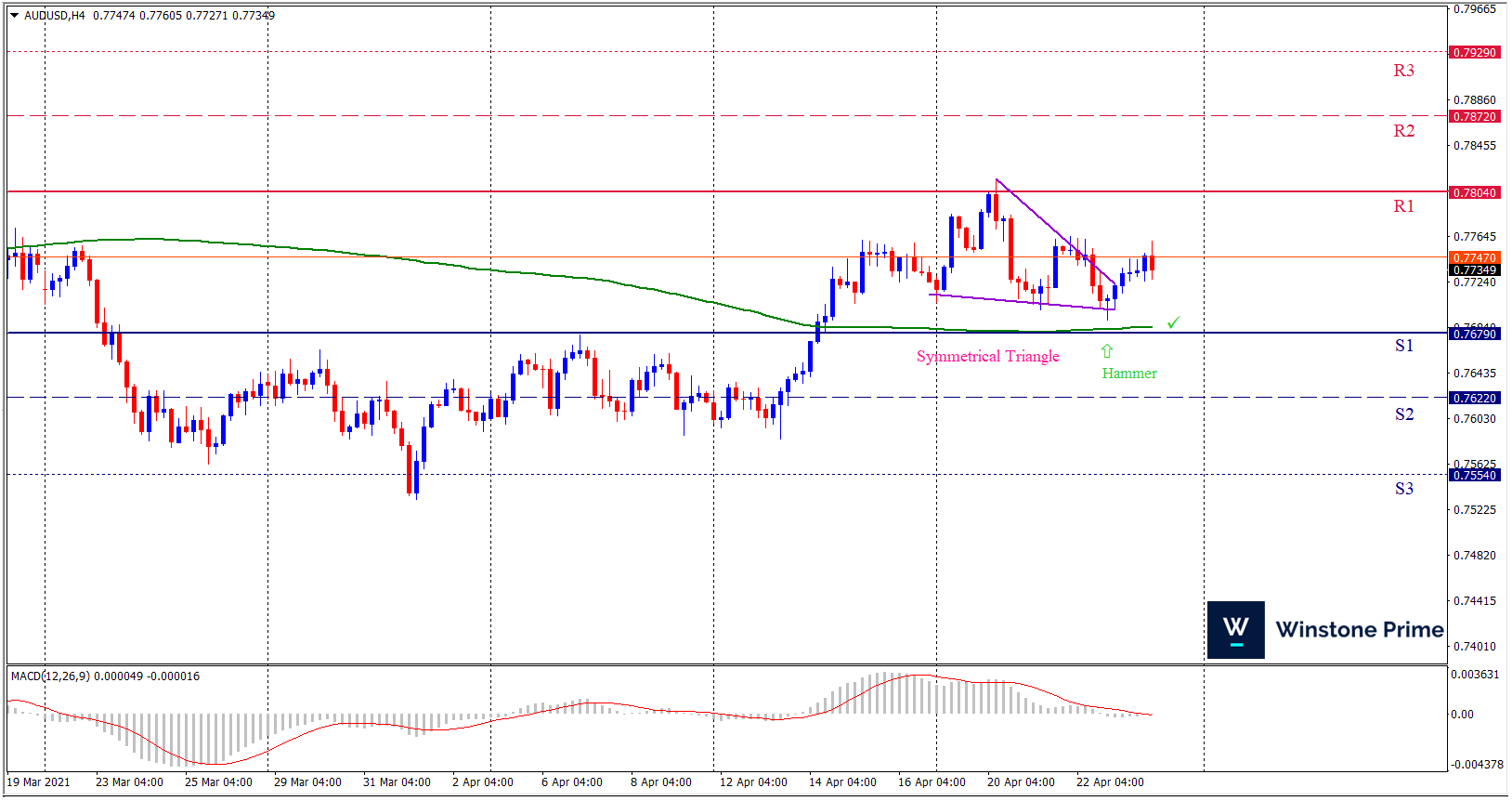

Technical View:

Last week’s high was 0.70% higher than the previous week. Maintaining high at 0.7816 and low at 0.7691 showed a movement of 125 pips.

In the upcoming week we expect AUD/USD to show a bullish trend. The currency pair is trading above the 200 Simple Moving Average and the MACD trades to the upside. A solid breakout above 0.7804 may open a clean path towards 0.7872 and may take a way up to 0.7929. Should 0.7679 prove to be unreliable support, the AUDUSD may sink downwards 0.7622 and 0.7554 respectively. In H4 chart symmetrical triangle breakout upside favors prospects of a bullish trend. Also to be noted Bullish hammer formation exerts the expectation of uptrend for the pair.

| Preference |

| Buy: 0.7728 target at 0.7851 and stop loss at 0.7674 |

| Alternate Scenario |

| Sell: 0.7674 target at 0.7555 and stop loss at 0.7728 |