The selling pressure in the US dollar pushes wake of delayed Fed taper’s talk. The dollar was brilliant on Tuesday following a one-day fall from May, despite traders being cautious in chasing a mood-driven move ahead of a Federal Reserve symposium to put an end to incentives and property purchases. The US data showed strong, but sluggish services and manufacturing activity overnight in Europe, while business activity growth in the United States slowed for the third month in a row due to the spread of the delta virus variant. For some investors, that casts enough uncertainty over the outlook to make it unlikely that the Fed delivers much of a signal at all during the symposium, putting pressure on the currency because it has gained with taper expectations.

Jackson Hole Symposium preview will be held on this month August and this year’s event, titled “Macroeconomic Policy in an Uneven Economy” will be held Thursday-Saturday, with Fed Chairman Powell’s keynote speech taking place at 10:00ET on Friday, August 27th. With the top policymakers from the ECB and Bank of England skipping this year’s event, traders’ focus will be almost exclusively on the US Federal Reserve, specifically any hints about the central bank’s timeline for tapering its asset purchases. Previous week’s FOMC minutes showed a split group, which preceded last month’s mix of optimism (strong NFP job report) and distrust (poor consumer sentiment, doubling of U.S. COVID cases). In that context, traders will be interested to see if Powell continues to hint at announcing Fed’s Taper plans after next month’s FOMC meeting, or if he will continue to sound more cautious, which will push traders back on their expectations.

Growth cooled for the third consecutive month in the United States, falling to its lowest level since December due to increased spread of delta variation due to material and labor restrictions and increasing viral infections. The service sector was severely affected by the increase in Covid cases, however production was severely curtailed and manufacturers lost momentum again unable to meet the strong demand.

On the other hand flash PMI surveys showed the eurozone enjoying the strongest expansion of the major developed economies in August. The eurozone is also benefitting from fewer supply and labour market constraints than the UK and US, where growth slowed sharply due to these shortages, with prices rising commensurately higher as a result. The eurozone enjoyed the fastest growth of the world’s major economies for a second month running in August, according to the flash PMIs, with growth slowing sharply in both the US and UK while Australia and Japan slipped into deeper downturns. Service sector growth held close to 15-year highs as lockdown measures were eased to the lowest since the pandemic began, helping offset some of the slowing in manufacturing, where eurozone producers reported ongoing supply constraints to have been a principal cause of weakened performance. The overall pace of manufacturing expansion nevertheless remained one of the strongest recorded over the past two decades.

The US dollar could also see a strong reaction to any unexpected comments. As for now, traders are waiting for the US Existing Home Sales data to trade fresh trading impetus and Europe GDP Quarterly report for further moment.

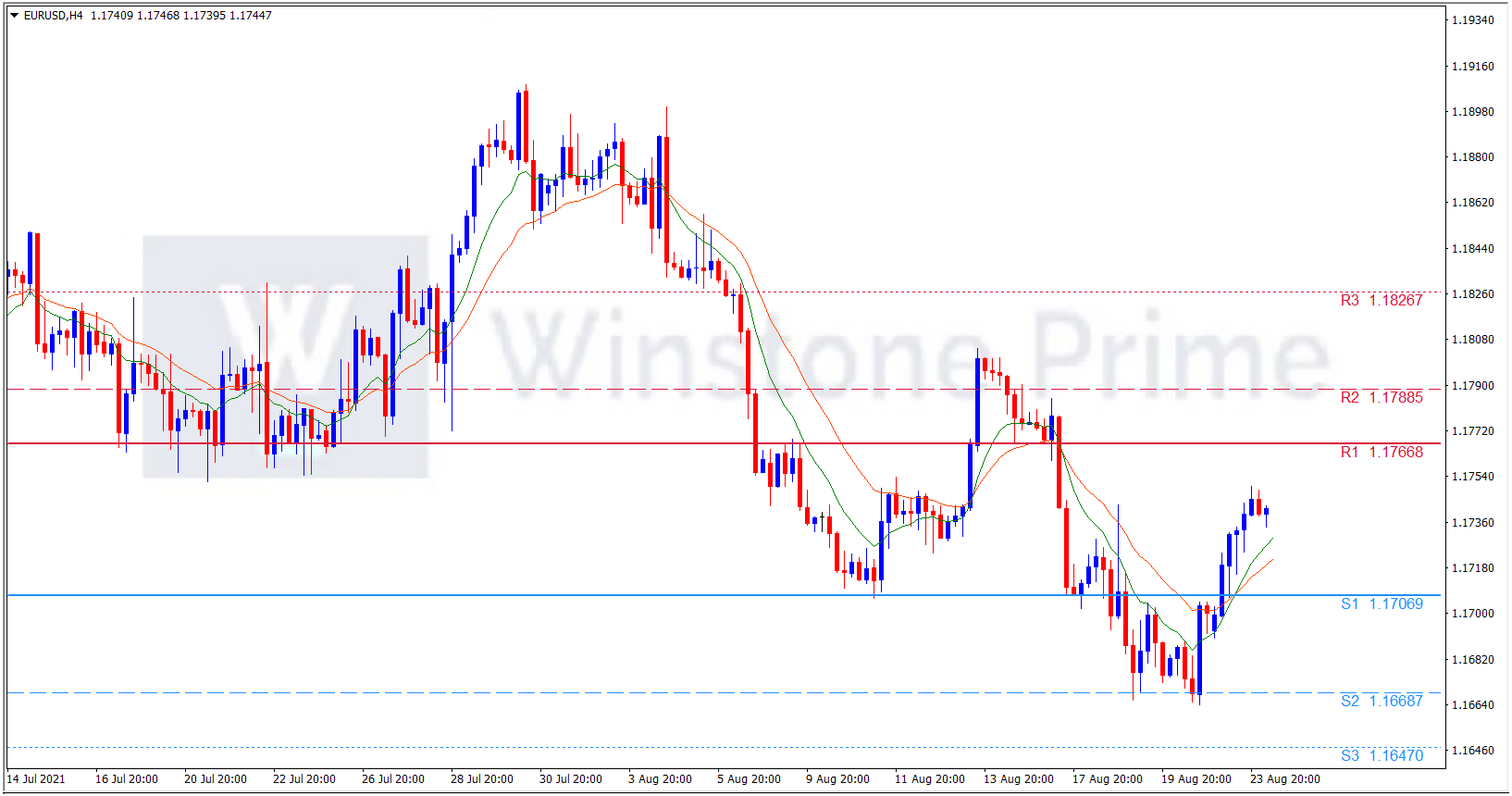

EUR/USD 4 Hour Chart:

Support: 1.1707 (S1), 1.1669 (S2), 1.1647 (S3).

Resistance: 1.1767 (R1), 1.1789 (R2), 1.1827 (R3).

Amidst this above catalysts US dollar soften moment and Europe yesterday PMI data kept the Euro pair into strong moment. We expect a bullish trend for EUR/USD.