The Greenback has gained some moment after the release of US CPI data yesterday. After several months of US inflation measurements, the August data offered some consolation for the “team transitory”, that the rise in prices caused by the reopening of the economy in the Federal Reserve and elsewhere will soon subside. Still, numbers do not solve the big inflation debate. Many economists point to persistent supply chain problems and rising wages as reasons for inflation to remain high for months to come.

The consumer price index rose 0.3% more than forecast since July, driven by a decline in used cars, airfares and auto insurance. Those divisions have been playing a key role in CPI molds in recent months. Annual inflation was 5.3%, down from an pandemic peak two months ago. Aneta Markovska the U.S. chief financial economist in Jefferies says that “It was a victory for the interim camp, but I do not think the debate is over.”. There are still a lot of reasons to expect higher inflationary pressures in the next three to six months.”

As per Bloomberg report “Snarled supply chains and shortages of materials -– two key drivers of pandemic inflation –- helped push prices for household furnishings up a record 1.2% last month. Food inflation remains elevated, and even with the smaller monthly gain in restaurant prices, diners are paying 4.7% more than they were a year ago. That’s likely because leisure and hospitality wages have risen 10.3% over that period, Andrew Hollenhorst and Veronica Clark, economists at Citigroup Inc., said in a note. A few categories in the latest CPI report showed limited inflation. Compared with August of last year, wireless telephone services posted the biggest decline since October 2019 and drug costs fell the most in six months”.

U.S. government bonds gained on expectations the August numbers will ease pressure on the Fed to start tightening monetary policy. Yields on 10-year treasuries are down and the central bank is will meet next week. The central bank will hold a two-day monetary policy meeting next week and investors are eager to know if an announcement will be made. The tapping dollar will benefit as the central bank points out that it is one step closer to a tight monetary policy. The central bank will buy less debt assets, which will effectively reduce the number of dollars in circulation. Investors coped with declining inflation and focused on the uncertainty about U.S. growth that is now clouded by the economic impact of the delta variation.

On the other hand, the measure of Australian consumer sentiment soared in early September, and the pace of vaccinations has increased significantly across the states as strict corona virus controls will soon be relaxed amid hopes. The Westpac-Melbourne Institute consumer sentiment index, released on Wednesday, rose 2.0% in September, rebounding a 4.4% fall in August. For those who have at least been fully vaccinated, sentiment in New South Wales rose 5.3% after the state government flagged the easing of restrictions in mid-October.

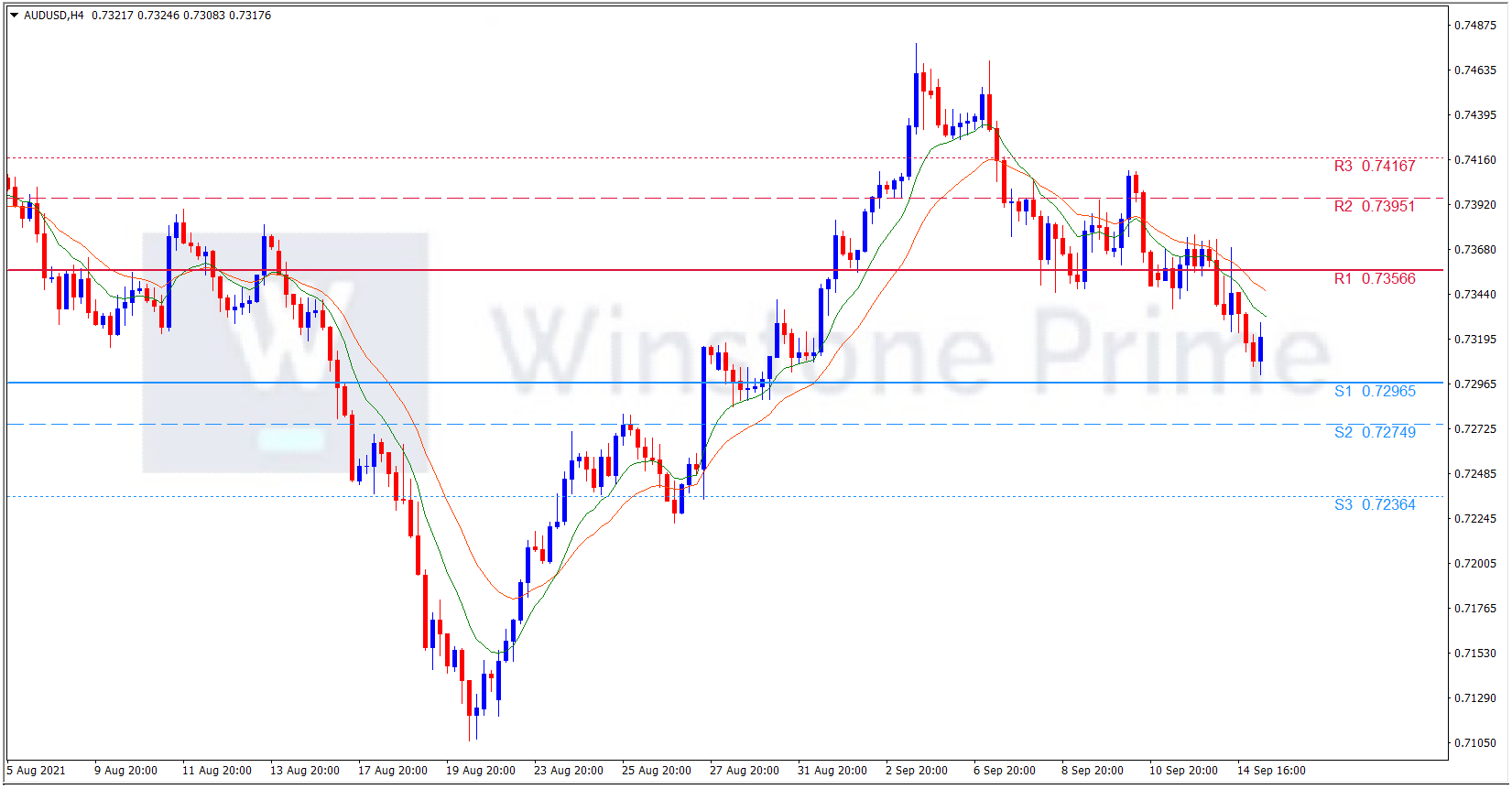

AUD/USD 4 Hour Chart:

Support: 0.7297 (S1), 0.7275 (S2), 0.7236 (S3).

Resistance: 0.7357 (R1), 0.7395 (R2), 0.7417 (R3).

Amidst this above catalysts the US dollar is on the uptrend among US CPI data. We expect a bearish trend for AUD/USD.