The dollar climbed to three-week peaks on Friday, still benefiting from better-than-expected U.S. retail sales data released on Thursday. The US dollar index (DXY) has peaked since August 23, rising last week as market sentiment soured. The US Federal Reserve (FED)’s tapping into this week’s Federal Open Market Committee (FOMC) may highlight the Covid – 19 fears and buzz as the main catalyst behind the moves. In addition, rising tensions between China and Western allies the United States, Australia and the United Kingdom also weigh on market sentiment and support the US dollar.

On the other hand the business community firmly believes that Europe must look to the future, even as they still manage the impact of the last 18 months. The European Commission’s renewed commitment to the political priorities set out before the pandemic for the 2019-2024 legislative term remain more relevant than ever and must be pursued resolutely, while factoring in the legacy of the deep economic crisis and the need to revive the European economy. The Malta Chamber, Eurochambres and many chambers across the EU made the case to public authorities and EU institutions for effective policies and to roll out funding support to aid millions of companies, without which they could not have survived. As we move beyond the crisis, it will be crucial to pursue the other important priorities that will contribute to a swift revival of the European economy.

It’s worth noting that the European Central Bank (ECB) policymakers seem divided over the future tapering of the bond purchases and rate hike, per their latest speech. The Fed, the European Central Bank and their peers in Japan, Britain and elsewhere brought down interest rates and unleashed huge asset-buying programmes last year to prevent an economic catastrophe. The Fed, which begins a two-day policy meeting on Tuesday, slashed rates to zero at the start of the pandemic in March 2020. To provide liquidity to the world’s biggest economy, it is buying at least $80 billion a month in Treasury debt and at least $40 billion in agency mortgage-backed securities.

The ECB has a 1.85-trillion-euro pandemic emergency purchase programme (PEPP), allowing the bank to buy assets in financial markets such as bonds, making their prices rise and interest fall. The ECB has kept the rate on its main refinancing operations at zero. Fed, ECB and BoE officials have insisted that inflation is only temporary and a consequence of prices recovering from drops at the height of the pandemic last year.

When Vice President Luis de Guindos suggested challenges to higher inflation and easy money, Governing Council member Gabriel Makhlouf said on Friday that the ECB would end the easing plan before raising interest rates, but declined to comment on the timing. In addition, board member Martins Kazak told Reuters, “(he) did not reach the 2% price target in the medium term.”

The greenback is benefiting from a risk-off mood and the German Producer Price Index (PPI) for August is disappointing with softer figures than expected at 0.8% and 1.9%. The reason may be linked to the Fed’s concern and uncertainty over US stimulus. Increasing confidence in the U.S. stimulus and expanding U.S. credit limits should not forget the slow but gradual economic recovery, brightening the central bank’s contradictions and favoring the pair bears.

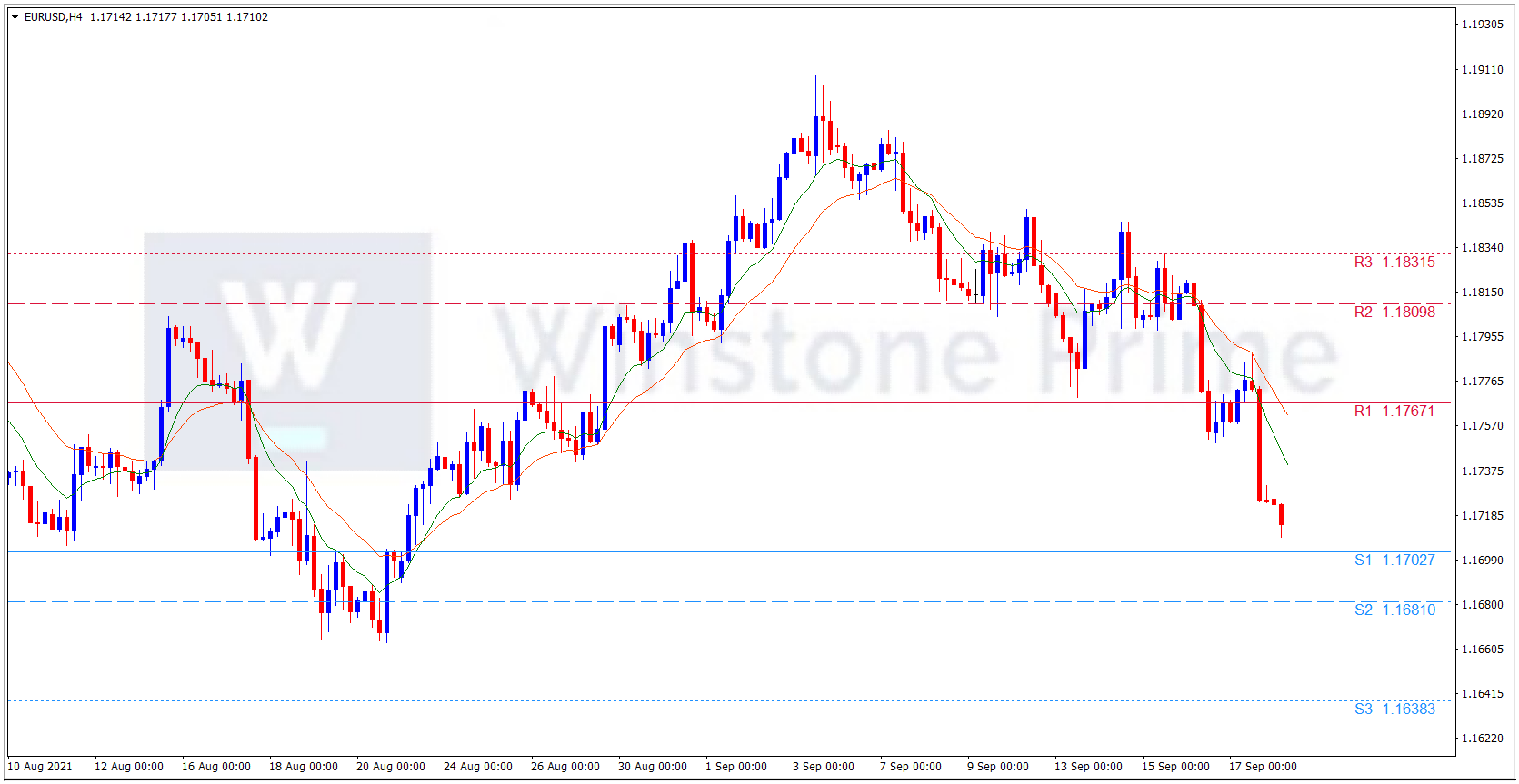

EUR/USD 4 Hour Chart:

Support: 1.1703 (S1), 1.1681 (S2), 1.1638 (S3).

Resistance: 1.1767 (R1), 1.1810 (R2), 1.1832 (R3).

Amidst this above catalysts the US dollar is benefiting from the Fed tapering. We expect a bearish trend for EUR/USD.