Fundamental view:

Aussie has bounced back and forth and closed the week forming a neutral candle. Demand for the American currency and plummeting equities has undermined the aussie whereas a nice comeback in gold prices partially offset their effects. Fed Chair Powell speech favored the greenback. The head of the Fed referred to stubbornly high inflation likely to extend into 2022, although he insisted it would likely be temporary. He commented that “the current inflation spike is really a consequence of supply constraints meeting solid demand, and that is all associated with the reopening of the economy, which is a process that will have a beginning, a middle and an end.” On the other hand, The Reserve Bank of Australia will have a monetary policy meeting on Tuesday, October 5. The central bank is widely anticipated to maintain the status quo, with action not expected until February 2022.

Australia RBA Private Sector Credit monthly report on 30th Sep and US ISM Manufacturing Employment on 1st Oct created bullish trend whereas US Goods Trade Balance on 28th Sep and US EIA Cushing Crude Oil Stocks Change on 29th Sep created bearish trend for the pair.

The major economic events deciding the movement of the pair in the next week are Australia Commonwealth Bank Services PMI, OPEC Meeting at Oct 01, RBA Interest Rate Decision, US ISM Non-Manufacturing PMI at Oct 05, US ADP Nonfarm Employment Change, US EIA Crude Oil Stocks Change at Oct 06, US Initial Jobless Claims at Oct 07 and US Nonfarm Payrolls at Oct 08.

AUD/USD Weekly outlook:

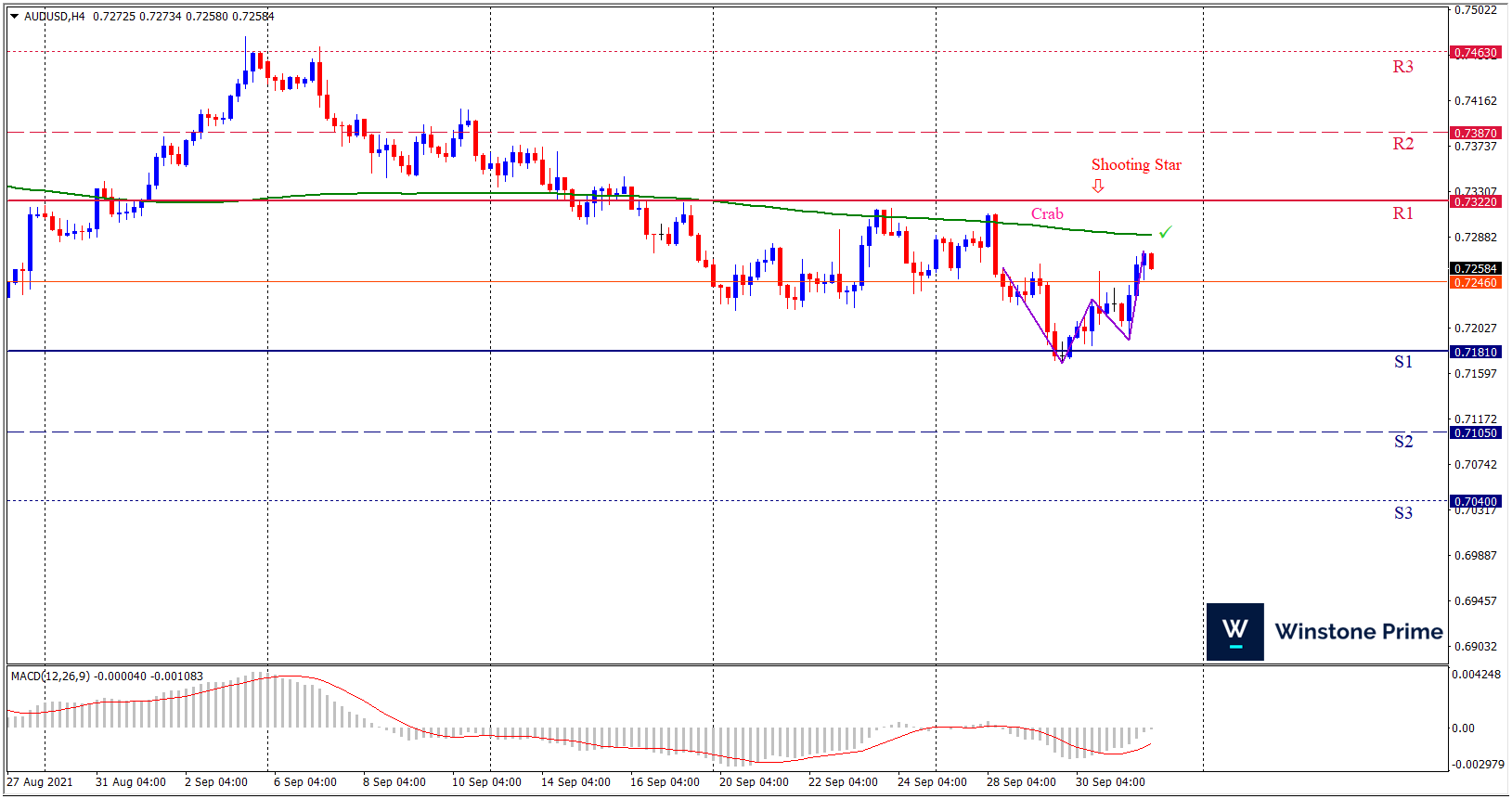

Technical View:

Last week’s high was 0.10% lower than the previous week. Maintaining high at 0.7310 and low at 0.7169 showed a movement of 141 pips.

In the upcoming week we expect AUD/USD to show a bearish trend. The currency pair is trading below the 200 Simple Moving Average and the MACD trades to the downside. A firm breakout below 0.7181 may create a fall towards 0.7105 and may take a way down to 0.7040. Should 0.7322 prove to be unreliable resistance, the AUDUSD may raise upwards 0.7387 and 0.7463 respectively. In H4 chart bearish crab pattern favors prospects of a bearish trend. And the shooting star formation provides a support on the expectation of downtrend for the pair.

| Preference |

| Sell: 0.7245 target at 0.7111 and stop loss at 0.7327 |

| Alternate Scenario |

| Buy: 0.7327 target at 0.7462 and stop loss at 0.7245 |