Fundamental view:

The British pound has went back and forth against the greenback during the trading course of the week. As far as central banks are concerned, It is expected that the Fed will double the pace of tapering to $30 billion a month. US policymakers will keep rates on hold, but pulling off support programs is the first step towards tightening, that means the chances of one or two rate hikes in 2022 have increased. On the other hand, All eyes are on the Bank of England’s decision on Thursday. Elsewhere, The sterling had already been under struggle with Johnson’s intentions to enact new restrictions in the face of rising COVID-19 cases in Britain. Waning immunity from vaccines, winter conditions and potentially a broader spread than the thought of the new Omicron variant are the main catalysts.

Positive update regarding the virus also joined in this week. The latest researches have suggested that Omicron is highly contagious but probably it is milder than previous variants. According to vaccine-makers Pfizer and BioNTech, three shots of their jab should provide sufficient protection.

Britain Markit/CIPS Construction PMI on 6th December and US CPI monthly report on 10th December framed downtrend whereas RICS House Price Balance on 9th December and Britain Manufacturing Production monthly report and Michigan Consumer Expectations on 10th December framed uptrend for the pair in this week.

The major economic events deciding the movement of the pair in the next week are UK Claimant Count Change at Dec 14, US Retail Sales monthly report, Fed Interest Rate Decision at Dec 15, BoE Interest Rate Decision, US Initial Jobless Claims, Fed Industrial Production monthly report at Dec 16, UK Retail Sales monthly report and Fed Governor Waller Speech at Dec 17.

GBP/USD Weekly outlook:

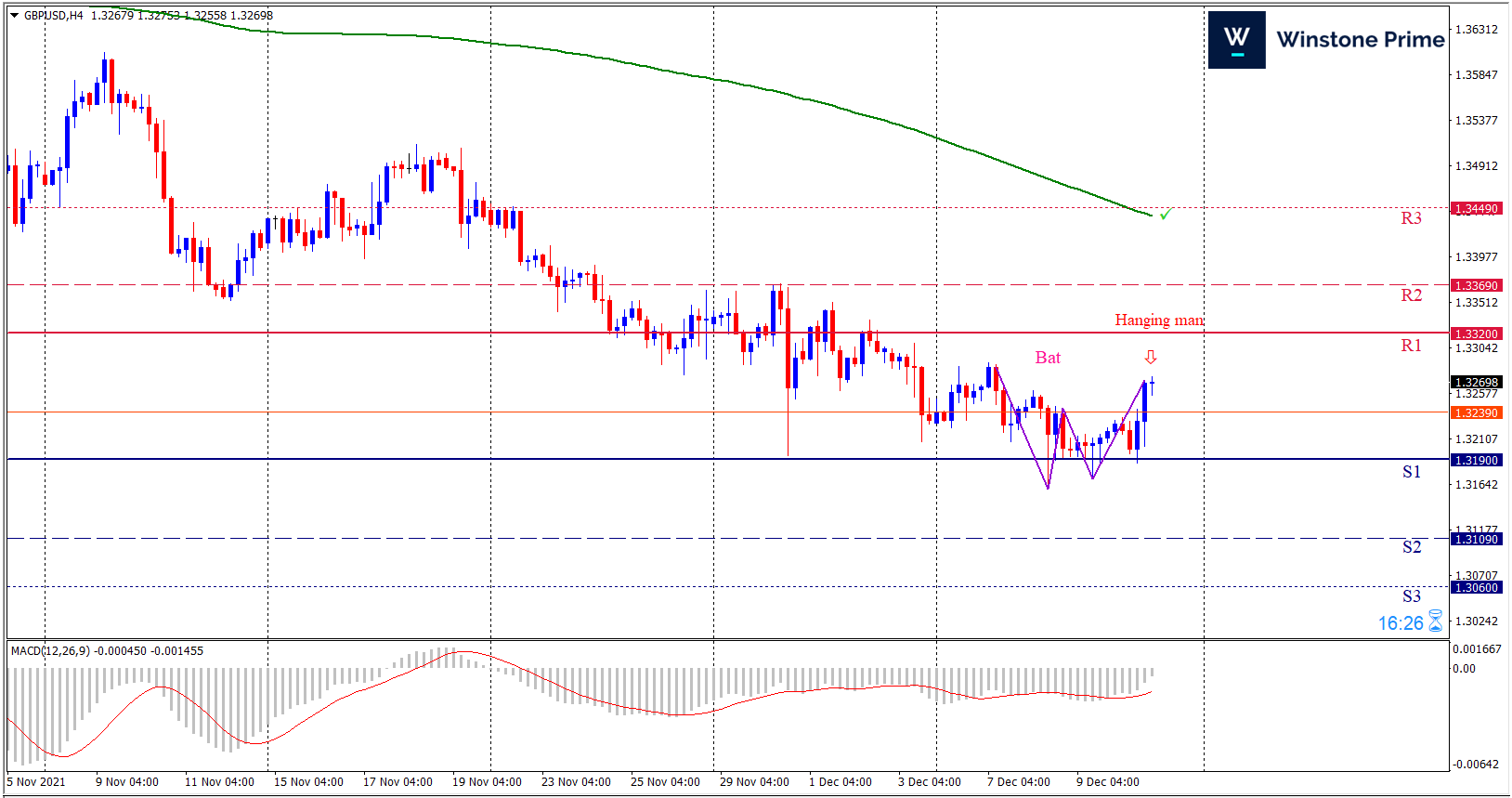

Technical View:

Last week’s high was 0.61% lower than the previous week. Maintaining high at 1.3289 and low at 1.3159 showed a movement of 130 pips.

In the upcoming week we expect GBP/USD to show a bearish trend. The currency pair is trading below the 200 Simple Moving Average and the MACD trades to the downside. Should 1.3190 proves to be unreliable support then the pair may fall further to 1.3109 and 1.3060 respectively whereas a solid breakout above 1.3320 will open a clear path upward to 1.3369 and then will further raise up to 1.3450. Chart formation of bearish bat pattern in H4 chart favors prospects of a bearish trend. Hanging man pattern formation further escalates the expectation for a bearish trend.

| Preference |

| Sell: 1.3265 target at 1.3141 and stop loss at 1.3325 |

| Alternate Scenario |

| Buy: 1.3325 target at 1.3448 and stop loss at 1.3265 |