Fundamental view:

The greenback initially rallied but later gave up gains against the Japanese yen during the trading course of the week. The most awaited Federal Reserve meeting since the November one, the Fed advanced it’s exit from pandemic support from June to March and tripled its 2022 rate hike forecast. The monetary policy was same as market expectations which produced negligible changes in the dollar. The Fed made an increment in the reduction in bond-buying on a monthly basis to $30 billion, from $15 billion as announced in November, starting from January 2022. Which means that the central bank will stop buying $20 billion Treasuries and $10 billion Mortgage-Backed Securities per month. The inflation forecasts have been raised to 5.6% for 2021 and 2.6% for 2022, up from 4.2% and 2.2% previously.

On the other hand, The Bank of Japan kept its overnight call rate at -01.%, completing its sixth year of negative rates, and reduced some of its pandemic business aid, again, to no market interest. While the Fed meeting dominating the market till Wednesday, the Rising covid cases of the recent variant Omicron bought the risk aversion sentiment back in the market which favored the Japanese yen off late.

BoJ Tankan Large All Industry Capex on 13th December and Philadelphia Fed Manufacturing Index on 16th December favored bearish trend whereas US Retail sales monthly report and EIA Crude Oil Stocks Change on 15th December and Japan Markit Manufacturing PMI on 16th December favored bullish trend for the pair in this week.

The major economic events deciding the movement of the pair in the next week are BoJ Monetary Policy Meeting Minutes at Dec 21, US GDP quarterly report, US CB Consumer Confidence Index, EIA Crude Oil Stocks Change at Dec 22, Japan Core CPI yearly report, US Core Durable Goods Orders monthly report, US Initial Jobless Claims and Michigan Consumer Sentiment at Dec 23.

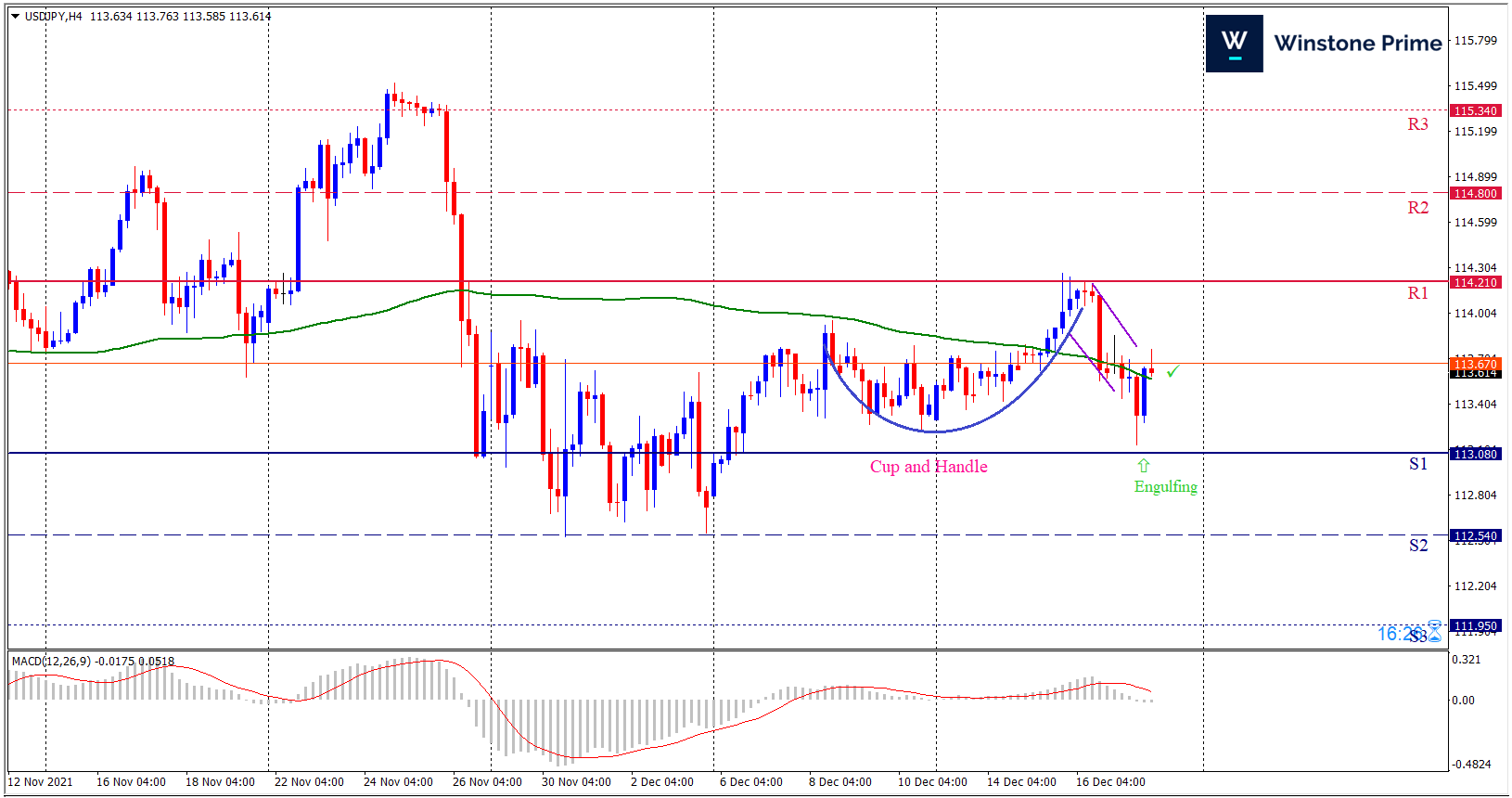

USD/JPY Weekly outlook:

Technical View:

Last week’s high was 0.28% higher than the previous week. Maintaining high at 114.27 and low at 113.14 showed a movement of 113 pips.

In the upcoming week we expect USD/JPY to show a bullish trend. The currency pair is trading above the 100 Simple Moving Average and the MACD trades to the upside. A solid breakout above 114.21 may open a clean path towards 114.80 and may take a way up to 115.34. Should 113.08 prove to be unreliable support, the USDJPY may sink downwards 112.54 and 111.95 respectively. In H4 chart, Formation of cup and handle pattern indicates reversal of the trend creating prospects of a bullish trend Along with a bullish engulfing formation braces our expectation.

| Preference |

| Buy: 113.69 target at 114.78 and stop loss at 113.03 |

| Alternate Scenario |

| Sell: 113.03 target at 111.96 and stop loss at 113.69 |