- Gold climbs up but it faces worst month in seven on U.S. rate hike bets.

- Mixed sentiment surrounding Ukraine war, China’s covid update dampens the market mood.

- US Treasury Sec. Yellen warns that more shocks likely to ‘challenge the economy’.

Gold prices rose on Friday due to worrying U.S. economic data rekindled some interest in the safe-haven yellow metal. However, Gold was still headed for its biggest monthly drop since September because of the fears of aggressive interest rate hikes by the Federal Reserve.

The disappointing US GDP data weighed on the US dollar. The GDP quarterly report came at -1.4% against the expectation of 7% and previous readout of 6.9%.

As per a currency strategist, “The disappointing U.S. GDP number could take some pressure off the Fed to tighten quite as aggressively as it has hinted, a rhetoric that has pressured gold in recent weeks,” “That has given gold a bit of a lifeline, and knocked the dollar back just a bit. I don’t expect these moves to continue though.”

Meanwhile, Fed officials have aligned around plans to accelerate the pace of interest rate hikes this year but remain split over what could be the make-or-break decision of where to stop to avoid dragging the economy into recession.

Mixed sentiment relating to the Russia-Ukraine crisis, as well as China’s covid woes seem to create cautious market mood among investors. Although private companies from the bloc are bracing for the Russian energy payment in the ruble, the bloc’s policymakers remain on their way to exerting more pressure on Moscow via an oil embargo.

As per AP News, US Treasury Secretary Janet Yellen warned Thursday that the coronavirus pandemic and the Russia-Ukraine war pose risks of big economic shocks, with downturns “likely to continue to challenge the economy.

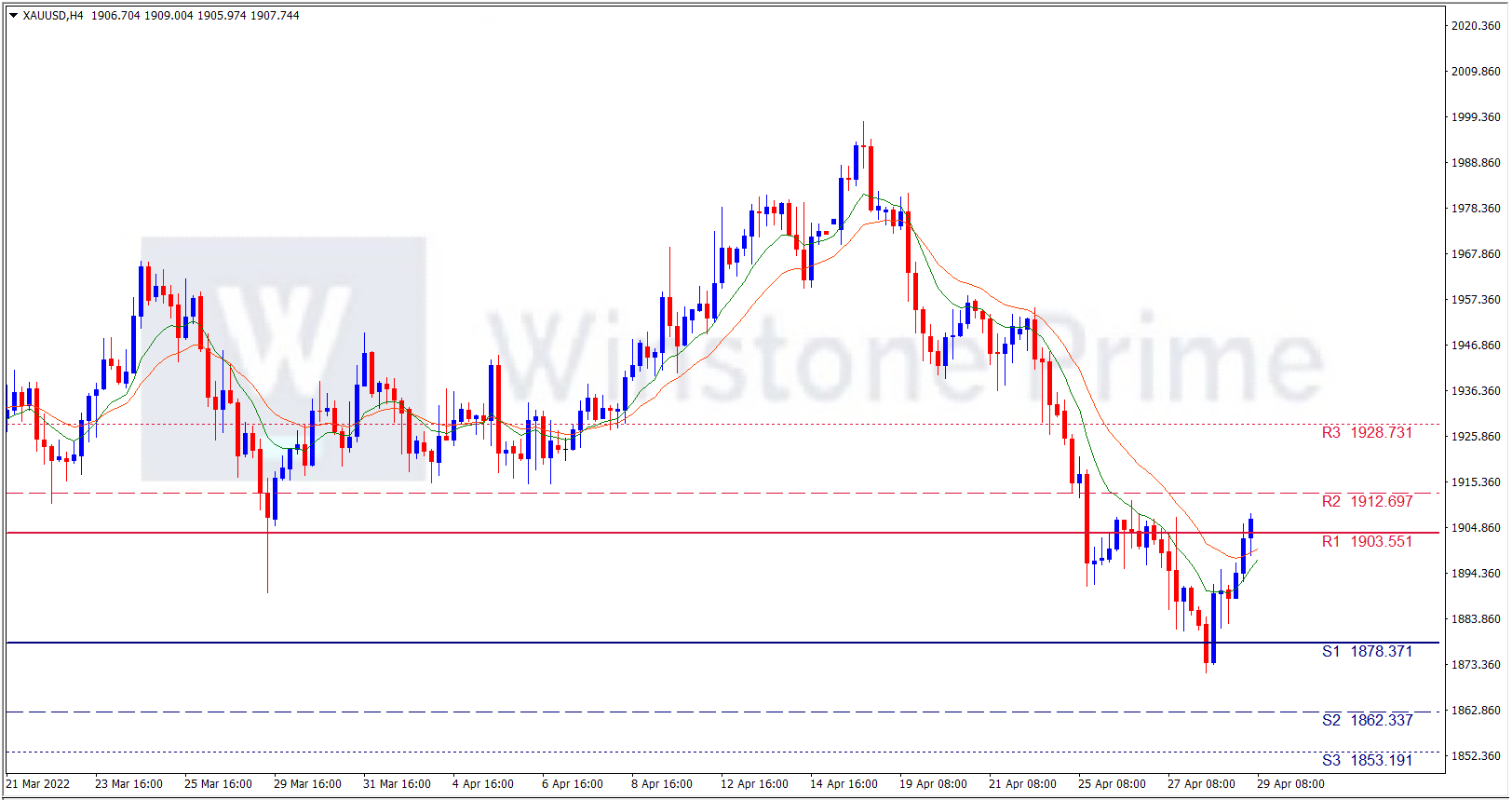

XAU/USD 4 Hour Chart:

Support: 1878.4 (S1), 1862.3 (S2), 1853.2 (S3).

Resistance: 1903.6 (R1), 1912.7 (R2), 1928.7 (R3).

Amidst all the catalysts creating cautious optimism for gold, we expect a bullish trend for XAU/USD.