Fundamental view:

The Euro plummeted against the US dollar during the trading course of the week. The geopolitical tension and the China’s covid-19 outbreak were the major catalysts in dampening the market mood, thus Investors flocked towards the safe-haven US dollar. Talking about geopolitical tension, the Russian gas supplier Gazprom halted exports to Bulgaria and Poland over failure to pay in rubles. Germany and Greece announced they might send additional gas to both countries, but EU representatives are generally considering the situation as an attempt at blackmail by Moscow which, for sure, will escalate tensions between the two economies.

Moving on to the central banks rate hikes, The US dollar was the most sought currency with aggressive Fed rate hike expectations, with the CME’s FedWatch tool showing a 96.5% probability of a 50 bps rate hike in May and a 85% chance of a 50 bps June lift-off. On the other hand, the ECB is barely planning to lift rates above 0% by that time, with the market anticipating three hikes, at the most, and gradual ones at that.

In this week, US Initial Jobless Claims on 28th April and France GDP quarterly report on 29th April creates bullish prospect whereas German Ifo Business Climate on 25th April and US Core Durable Goods Orders monthly report on 26th April creates bearish prospect for the pair.

The major economic events deciding the movement of the pair in the next week are US ISM Manufacturing PMI at May 02, Eurozone Unemployment Rate, ECB President Lagarde Speech at May 03, ECB Non-monetary Policy Meeting, US ADP Nonfarm Employment Change, US ISM Non-Manufacturing PMI, EIA Crude Oil Stocks Change, Fed Interest Rate Decision at May 04 and Nonfarm Payrolls at May 06.

EUR/USD Weekly outlook:

Technical View:

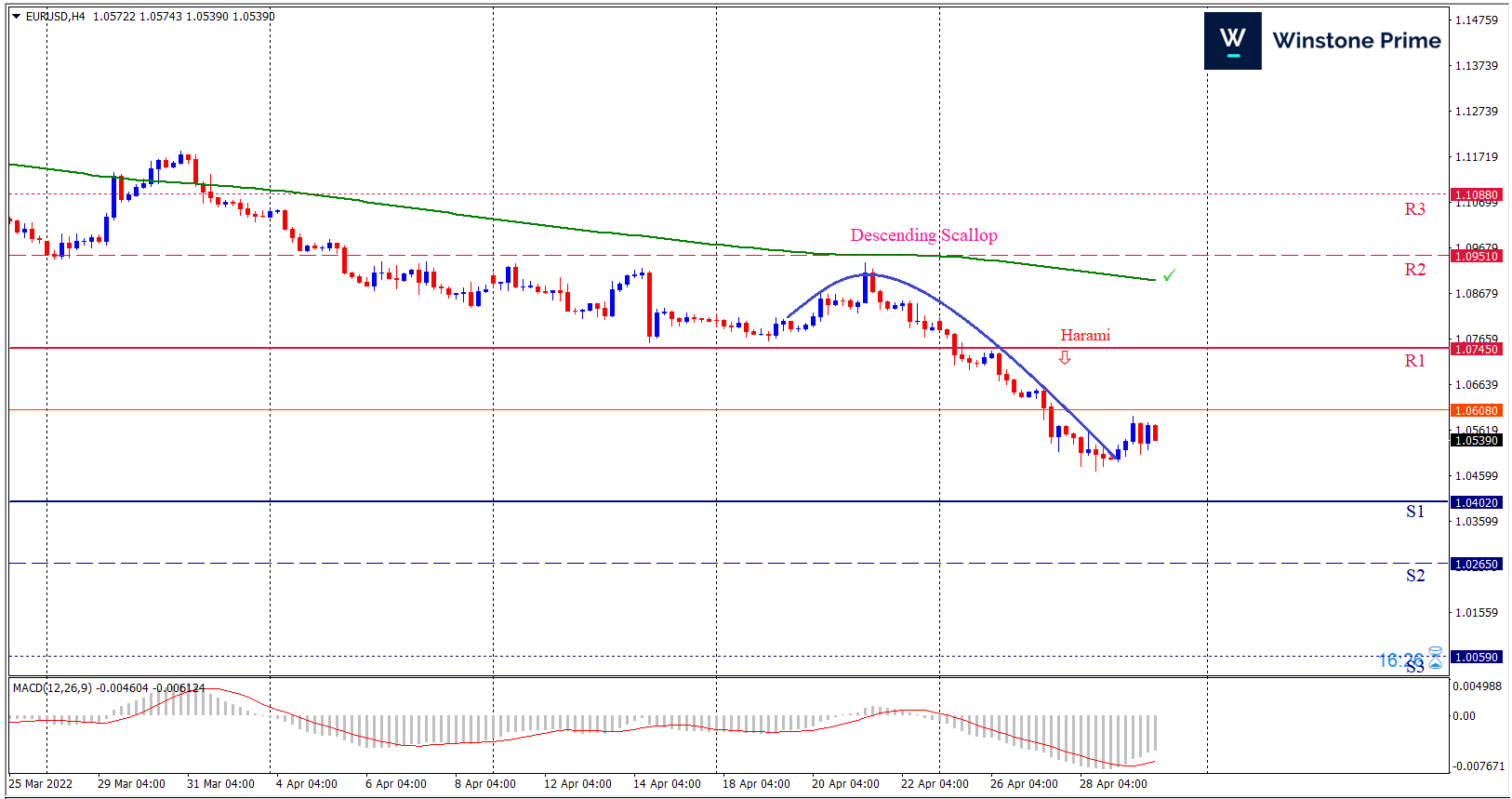

Last week’s high was 1.12% lower than the previous week. Maintaining high at 1.0814 and low at 1.0471 showed a movement of 343 pips.

In the upcoming week we expect EUR/USD to show a bearish trend. The currency pair is trading below the 200 Simple Moving Average and the MACD trades to the downside. Should 1.0402 proves to be unreliable support then the pair may fall further to 1.0265 and 1.0059 respectively whereas a solid breakout above 1.0745 will open a clear path upward to 1.0951 and then will further raise up to 1.1088. Chart formation of a descending scallop pattern in H4 chart sets prospects for a bearish trend. Bearish harami formation in H4 chart escalates the expectation for a bearish trend.

| Preference |

| Sell: 1.0539 target at 1.0267 and stop loss at 1.0750 |

| Alternate Scenario |

| Buy: 1.0750 target at 1.1087 and stop loss at 1.0539 |