Fundamental view:

The Australian dollar had a bearish momentum against the American dollar during the trading course of the week. The hawkish Fed and the risk off market mood favored the US dollar. The Russia – Ukraine crisis and the coronavirus returning to China walloped the market sentiment. Market Participants has priced a 70% chance of double-dose Fed rate hikes in May and June after US inflation soared to a four-decade high of 8.5% in March. And St. Louis Fed President James Bullard made a case for a 75 bps rate hike if needed. Fed Jerome Powell endorsed front-loading rate hikes, confirming a 50 bps lift-off in May.

Meanwhile, The Reserve Bank of Australia has recently came in to the hiking arena, as in its latest monetary policy meeting, policymakers opened the door for a rate move. As of now, the central bank is expected to hike some 40 bps by June. Still, it is way behind the US Federal Reserve, which is expected to push rates towards the 2.75%-3% range by the end of the year, that is a another reason for the Aussie slide.

In this week, US Initial Jobless Claims on 21st April and Australia S&P Global Manufacturing PMI on 22nd April underpinned bullish trend whereas US EIA Crude Oil Stocks Change on 20th April, Fed powell speech on 21st April and Australia S&P Global Services PMI on 22nd April underpinned bearish trend for the quote.

The major economic events deciding the movement of the pair in the next week are US Core Durable Goods Orders monthly report, US CB Consumer Confidence Index at Apr 26, RBA Weighted Median CPI quarterly report at Apr 27, US GDP quarterly report, US Initial Jobless Claims at Apr 28, Australia PPI quarterly report, US Employment Cost Index quarterly report and Michigan Consumer Sentiment at Apr 29.

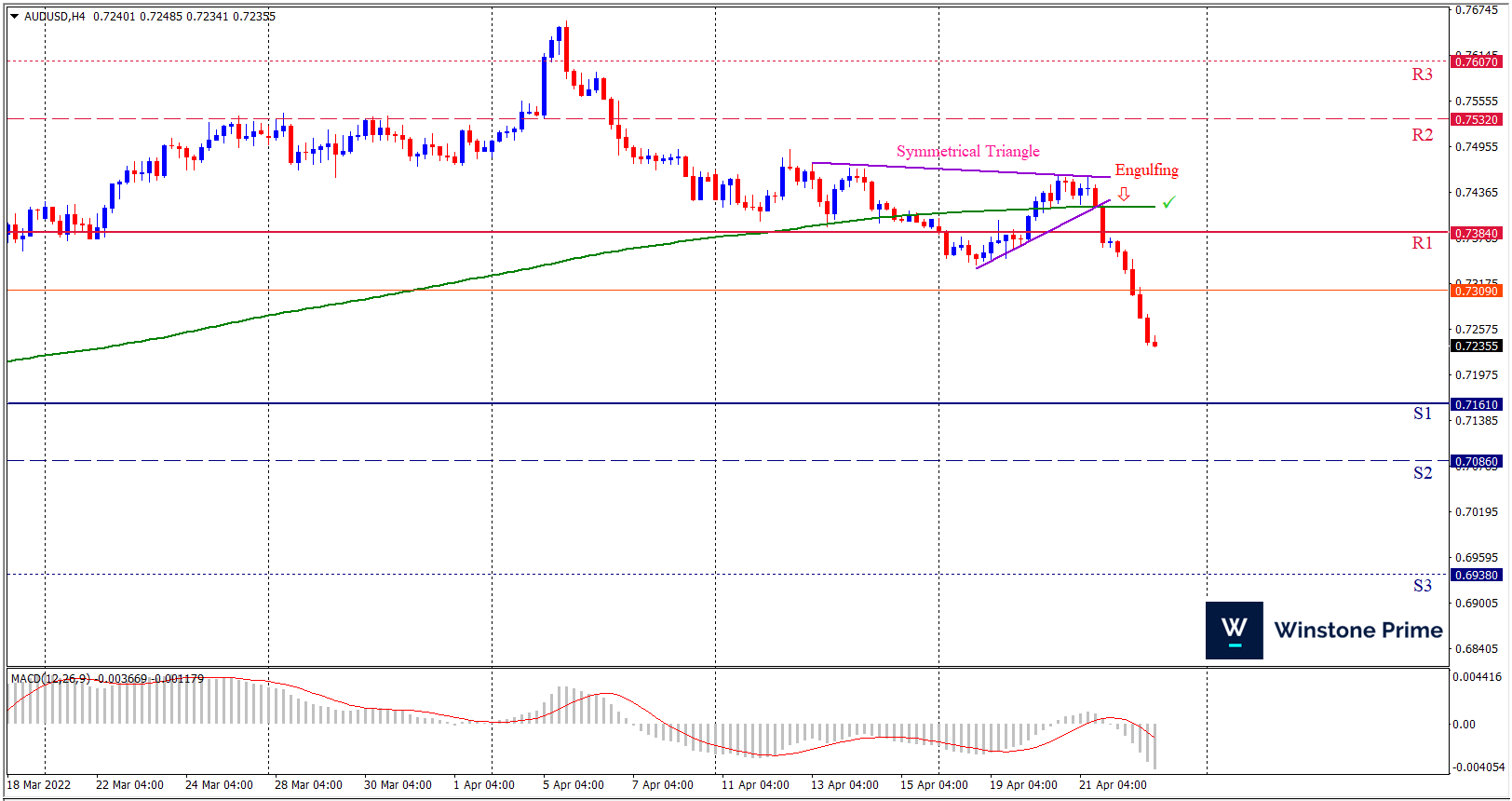

AUD/USD Weekly outlook:

Technical View:

Last week’s high was 0.48% lower than the previous week. Maintaining high at 0.7457 and low at 0.7234 showed a movement of 223 pips.

In the upcoming week we expect AUD/USD to show a bearish trend. The currency pair is trading below the 200 Simple Moving Average and the MACD trades to the downside. Should 0.7161 proves to be unreliable support then the pair may fall further to 0.7086 and 0.6938 respectively whereas a solid breakout above 0.7384 will open a clear path upward to 0.7532 and then will further raise up to 0.7607. In H4 chart symmetrical triangle breakout downside favors prospects of a bearish trend. Also to be noted bearish engulfing formation exerts the expectation of downtrend for the pair.

| Preference |

| Sell: 0.7235 target at 0.7049 and stop loss at 0.7389 |

| Alternate Scenario |

| Buy: 0.7389 target at 0.7605 and stop loss at 0.7235 |