Today Bank of Japan board member Toyoaki Nakamura warned of the risks to the economic outlook posed by the recent rise in the Covid-19 pandemic, but expressed hope that consumption would increase once homes felt safe to spend. Nakamura said the world’s third-largest economy would recover as the impact of the pandemic fades, encouraging growth from strong global demand and pointing to a recovery in capital spending. Risks of “highly uncertain” bent forward as the emergency situation to fight the epidemic hurts retailers, the former corporate executive said.

But Nakamura signalled hope that once vaccinations proceed, consumption may get a boost from pent-up demand with Japanese households having loaded up a record 1,056 trillion yen ($9.61 trillion) in cash and deposits. Nakamura said in a speech that “the resurgence in infections may have somewhat delayed the timing for when pent-up demand materialises,” and added there was a chance economic activity may strengthen more than expected once the pandemic’s impact eases.

Japan wants to extend the state of emergency to eight more provinces, taking the total to 21, to prevent a rapid increase in corona virus infections, said the minister in charge of anti-Covid. After Japan’s economy collapsed in the first three months of this year, higher than expected in the second quarter, a symptom is that consumption and capital expenditure are recovering from the initial success of the corona virus epidemic. Some of the researchers expect growth to be moderate in the current quarter as controls are re-expended to control the increase in infections.

Risk appetite in global markets has strengthened since the U.S. Food and Drug Administration granted full approval to the COVID-19 vaccine developed by Pfizer PFE.N and BioNTech 22UAy.DE in a move that could accelerate U.S. inoculations. The United States could get COVID-19 under control by early next year, Dr. Anthony Fauci, the country’s top infectious disease expert, said on Tuesday.

The greenback has rallied in recent weeks, with the dollar index hitting a 9 1/2-month high of 93.734 on Friday, not just on fear about Delta’s economic impact, but also an the Federal Reserve signalled a tapering of stimulus was likely this year.

The US economy is putting out a lot of mixed signals and the Delta variant is weighing on economic data and consumer sentiment, the recovery is still chugging along and plenty of businesses remain optimistic about the future. Investors awaited Federal Reserve Chairman Jerome Powell’s speech this week for guidance on the central bank’s taper plans. The coronavirus curve in some hotspots is easing and the U.S. Food and Drug Administration’s approval of vaccinations. The U.S. drug regulator granted full approval on Monday to the Pfizer /BioNTech COVID-19 vaccine, raising hopes inoculations could accelerate. Risk sentiment was also underpinned by remarks from top U.S. infectious disease expert Dr. Anthony Fauci that the nation could get COVID-19 under control by early next year if vaccinations ramp up.

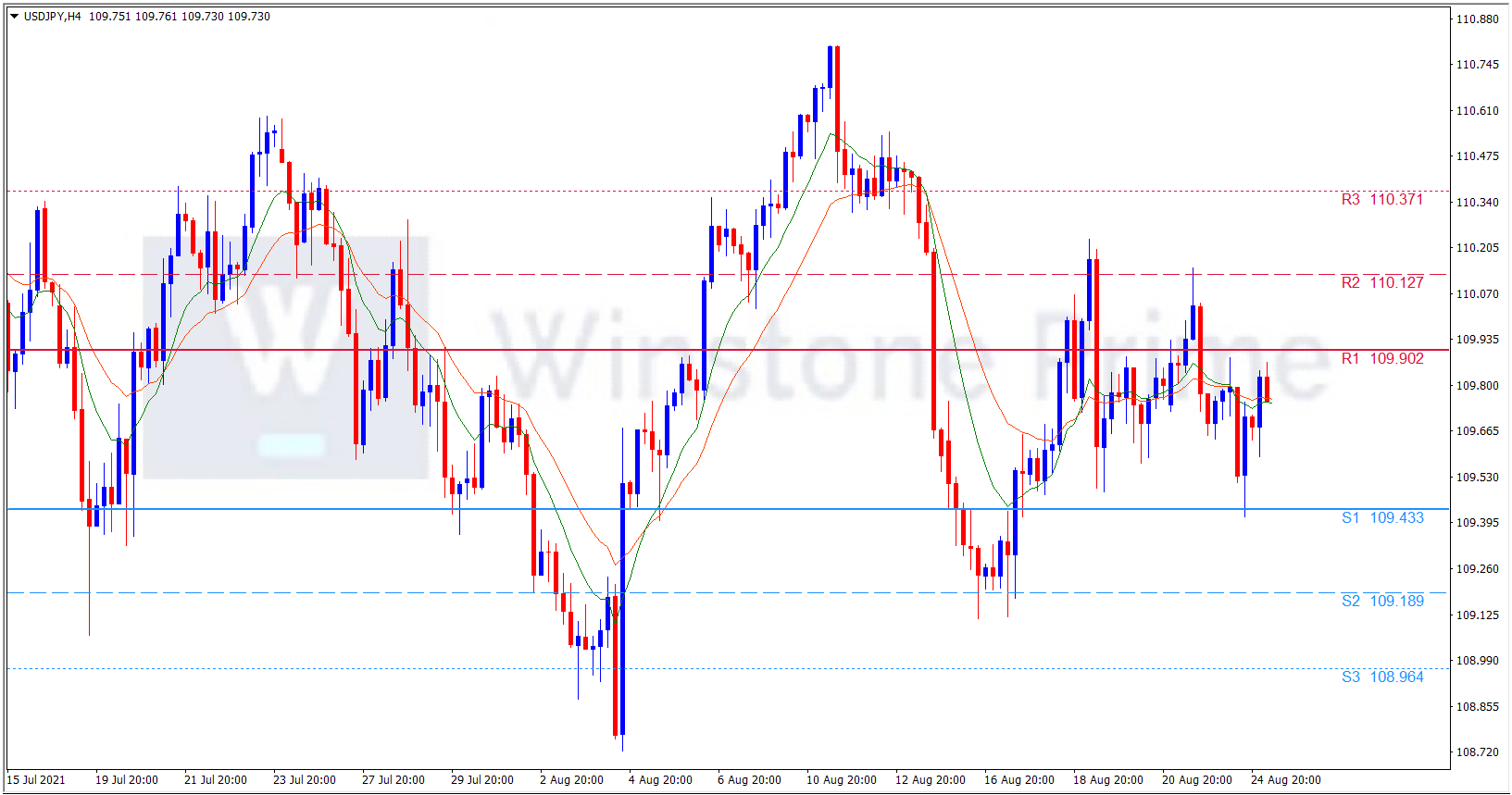

USD/JPY 4 Hour Chart:

Support: 109.43 (S1), 109.19 (S2), 108.96 (S3).

Resistance: 109.90 (R1), 110.13 (R2), 110.37 (R3).

Amidst this above catalysts the dollar is on uptrend today. We expect a bullish trend for USD/JPY.