Fundamental view:

The US dollar has fallen a bit during the course of the trading week. The USD/JPY is lower on the week, stocks had a fall on Thursday and Treasury yields have been sliding since the Fed meeting on June 16. The expectations for a powerful US rebound have been so overstated that a more realistic view was probably inevitable. Whereas Japan’s data gave scant evidence that the island economy is improving.

Japan Coincident Index on 7th July and Japan BoJ M2 Money Stock yearly report on 9th July framed uptrend whereas Japan Household Spending yearly report on 6th July and Japan Economy Watchers Sentiment on 8th July created downtrend for the pair.

The major economic events deciding the movement of the pair in the next week are US WASDE Report at July 12, US Federal Budget Balance at July 13, Japan Industrial Production monthly report, US Fed Chair Powell Testimony at July 14, Japan Tertiary Industry Activity Index monthly report, US Initial Jobless Claims at July 15, BoJ Interest Rate Decision and US Retail sales monthly report at July 16.

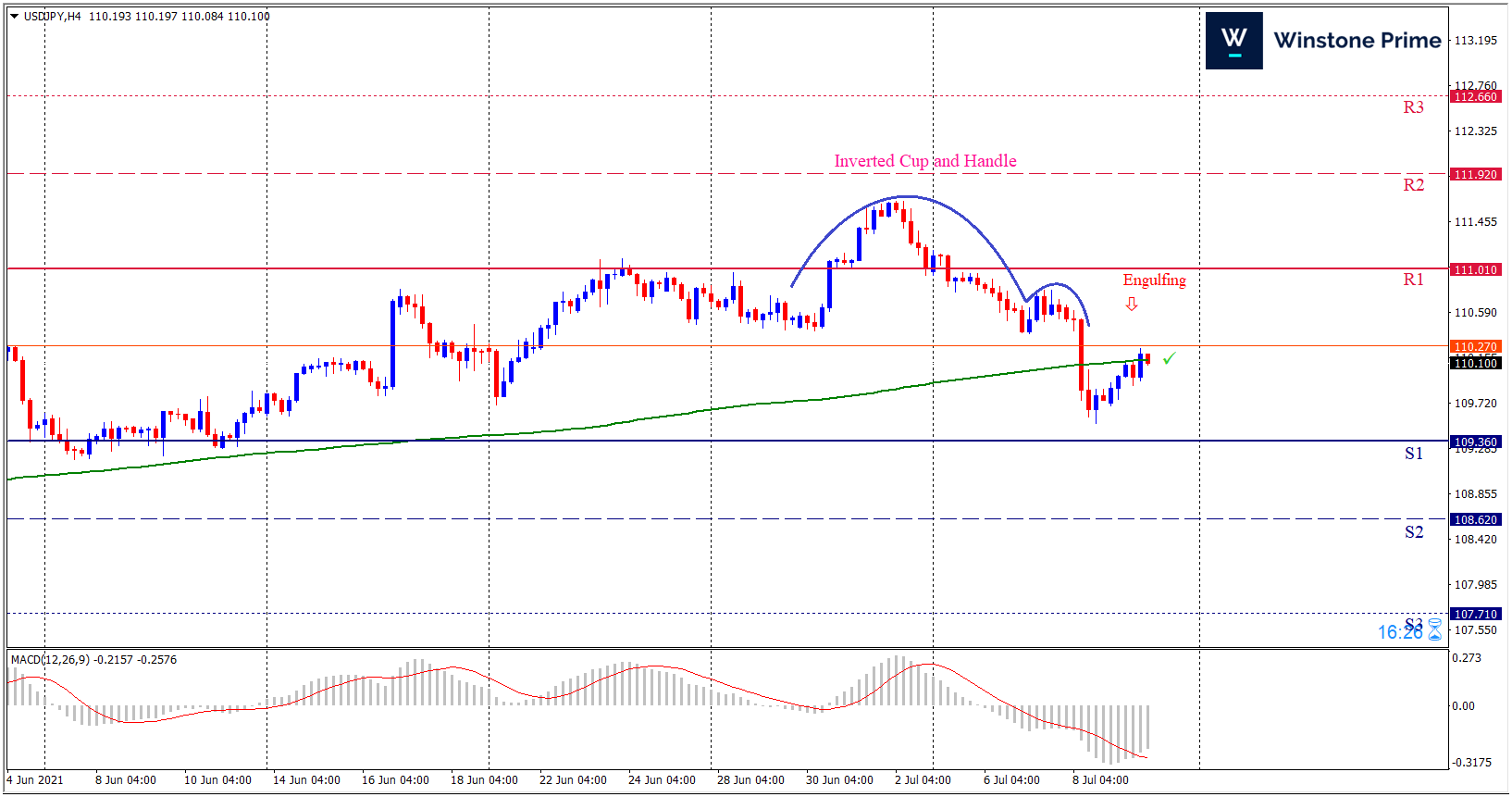

USD/JPY Weekly outlook:

Technical View:

Last week’s high was 0.42% lower than the previous week. Maintaining high at 111.18 and low at 109.53 showed a movement of 165 pips.

In the upcoming week we expect USD/JPY to show a bearish trend. The currency pair is trading below the 200 Simple Moving Average and the MACD trades to the downside. A solid breakout below 109.36 may open a clean path towards 108.62 and may take a way down to 107.71. Should 111.01 prove to be unreliable resistance, the USDJPY may raise upwards 111.92 and 112.66 respectively. In H4 chart, Formation of inverted cup and handle pattern indicates reversal of the trend creating prospects of a bearish trend Along with a bearish engulfing formation braces our expectation.

| Preference |

| Sell: 110.11 target at 108.63 and stop loss at 111.06 |

| Alternate Scenario |

| Buy: 111.06 target at 112.65 and stop loss at 110.11 |