In an interview, on the sidelines of the Mines and Money Online Connect Global mining conference, the celebrated fund manager said that while he is no fan of the Federal Reserve, he sees that they are in an untenable position as they try to support the U.S. economy as it continues to feel the significant effects of the COVID-19 pandemic.

He added that “to promote growth, the U.S. central bank will continue to be forced to keep interest rates low and that will drive gold prices higher.” “Understand negative, real interest rates for what they are: they’re a war one on savers by spenders. And in a democracy, the winner of that war is foreshadowed given that the spenders are so much more numerous than savers. So from a political point of view, the Fed is doing the only thing that it can do,” he said. I don’t see what their way out is.”

Adding to it, U.S. job growth likely slowed further in August as financial assistance from the government ran out, threatening the economy’s recovery from the COVID-19 recession. The Labor Department’s closely watched employment report on Friday would come as companies from transportation to manufacturing industries announce layoffs or furloughs. It could add pressure on the White House and Congress to restart stalled negotiations for another fiscal package, and will likely become political ammunition for both Democrats and Republicans with just two months to go until the presidential election.

Lydia Boussour, a senior economist with Oxford Economics in New York, estimated that payroll gains in line with expectations would leave one out of two laid-off workers still unemployed, with an increased risk of a prolonged high unemployment spell.

“The fact that the employment is settling into a trend of slow, grinding improvement is a worrisome sign for the broader recovery,” said Boussour. “The combination of slow employment progress and poor health conditions along with the absence of fiscal aid risk jeopardizing the consumer spending rebound in the coming months.”

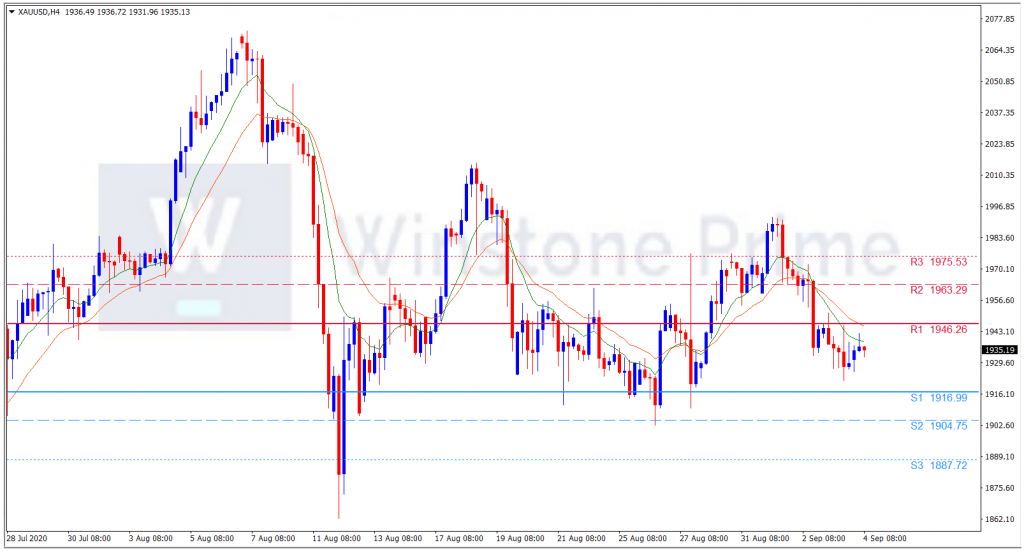

XAU/USD 4 Hour Chart:

Support: 1917.0 (S1), 1904.8 (S2), 1887.7 (S3).

Support: 1917.0 (S1), 1904.8 (S2), 1887.7 (S3).

Resistance: 1946.3 (R1), 1963.3 (R2), 1975.5 (R3).

Amidst all the opinions coming against the greenback, the yellow metal bulls remain unnerved. But whether the upcoming US Non-farm payrolls data due to be published later on Friday at 12:30 GMT will add temporary strength to the greenback is yet to be seen. We expect a bullish trend for XAU/USD.