Japan’s Nikkei inches low ahead of today’s US Federal Reserve (Fed) monetary policy meeting in Wednesday Asian session. The US dollar is showing gains as investors looked towards a key Federal Reserve policy meeting to see if it would reinforce growing market expectations for earlier rate rises next year.

Bank of Japan Governor Haruhiko Kuroda said on Wednesday consumer inflation may approach its 2% inflation on rising raw material costs, offering his clearest signal to date that upward price pressures will continue to broaden.

But he also added that the central bank would maintain its ultra-loose monetary policy to ensure any rise in prices would be accompanied by higher wages and a recovery in the economy.

“It’s true there’s a chance consumer inflation will approach 2% through various channels,” Kuroda told parliament. “But what’s desirable is for the economy to recover steadily and push up corporate profits, thereby leading to higher wages and inflation. We’ll patiently maintain ultra-easy policy to achieve this at the earliest date possible,” he said.

Elsewhere, The Bank of Japan on Wednesday showed readiness to pump 2 trillion yen ($17.6 billion) into markets through temporary government bond purchases to counter a recent rise in short-term interest rates.

Moreover, Japan PM Fumio Kishida accepts mistakes in the Construction Orders data but turns down any impact of the mistakes on GDP for FY 2020 and 2021.

On the other hand, Markets have been pricing for the Fed to wrap up bond-buying around March and then proceed with one or maybe two rate hikes in 2022. Elsewhere The US Senate approved a bill to raise the debt ceiling by $2.5 trillion whereas President Joe Biden also sounds hopeful of getting his Build Back Better (BBB) plan through the House in 2021.

However, the rapid spread of the Omicron adds pressure that could incline the Fed to be less hawkish, but recently officials have sounded more concerned about the persistence of inflation than the pandemic. Whatever the Fed decides will set the bar for the central banks of the EU, UK and Japan when they meet this week, and add to pressure for further tightening in emerging markets.

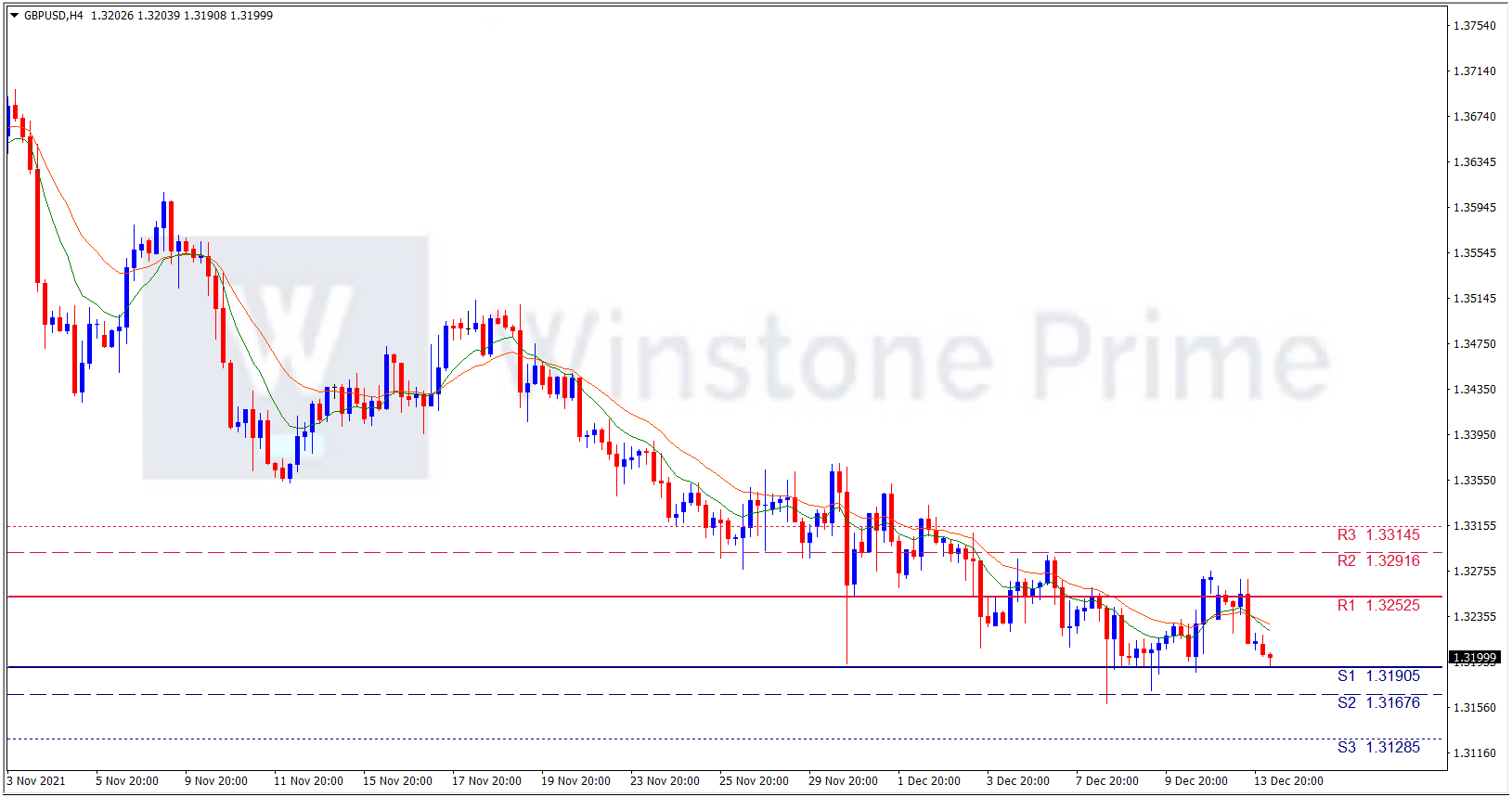

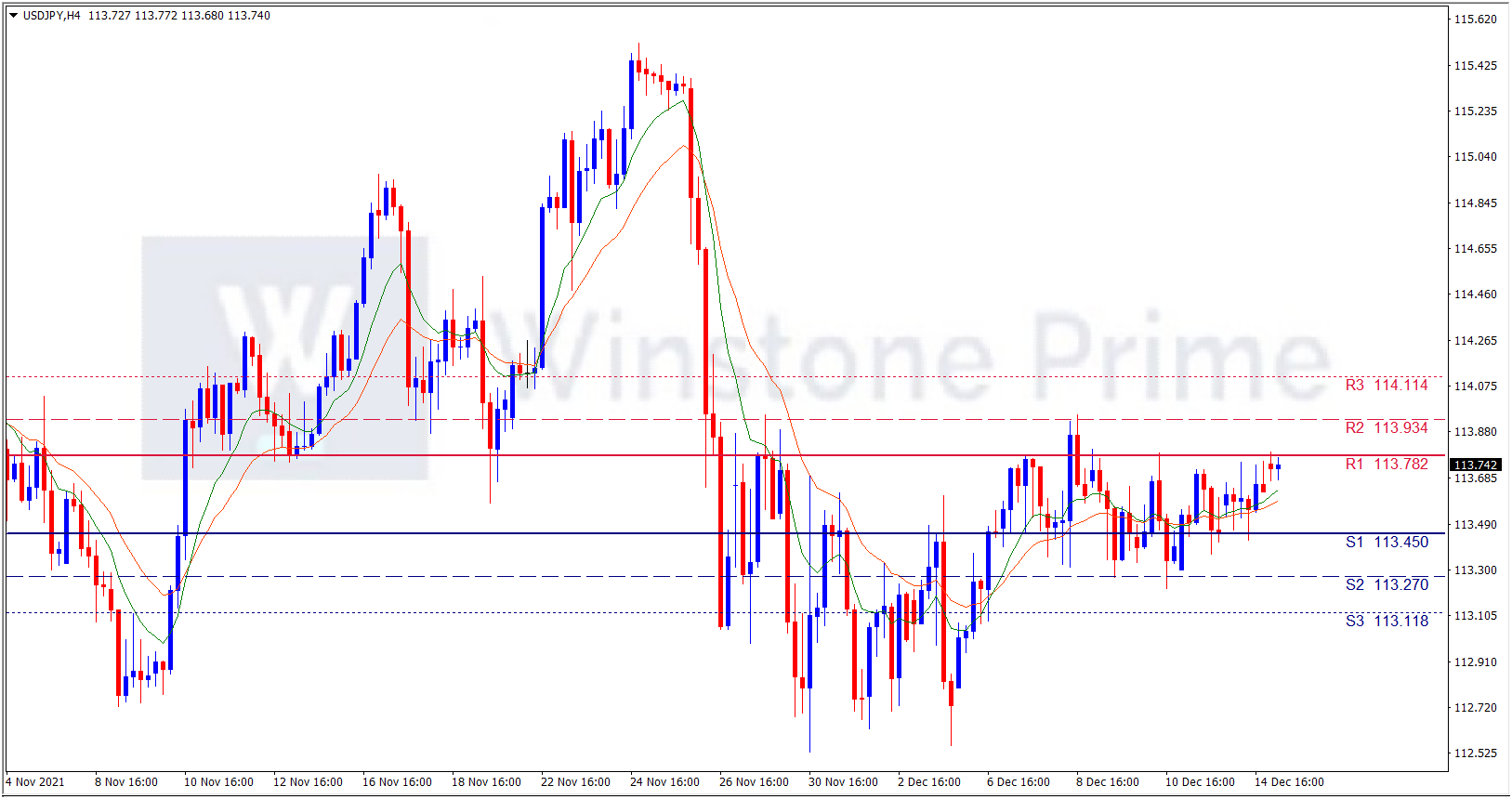

USD/JPY 4 Hour Chart:

Support: 113.45 (S1), 113.27 (S2), 113.12 (S3).

Resistance: 113.78 (R1), 113.93 (R2), 114.11 (R3).

The hawkish expectation from Fed amidst the omicron woes creates cautious optimism among the USD/JPY traders. We expect a bullish trend for USD/JPY.