Fundamental view:

The British pound has gone back and forth against the greenback during the course of the week. Long term US government bond yields showed decline last week. The benchmark on the 10-year Treasury note fell to 1.51%, while that on the 2-year bond has surged above 0.50%. A narrowing spread usually hints at a rate-hiking cycle but also suggests slowing economic growth. This gap between near-term and long-term bond yields is not only seen in the US but also similar in Germany, the UK, Canada and Australia, particularly when comparing 5-year and 30-year bond yields. The US Federal Reserve will have meeting next week, announcing the outcome on Wednesday, November 3.

BoE MPC Member Tenreyro Speech on 25th October and Britian 5-Year Treasury Gilt Auction on 26th October framed bullish trend whereas CB Consumer Confidence Index on 26th October and Baker Hughes US Oil Rig Counton 29th October framed bearish trend for the pair.

The major economic events deciding the movement of the pair in the next week are UK Markit/CIPS Manufacturing PMI, US ISM Manufacturing PMI at Nov 01, US ADP Nonfarm Employment Change, Fed Interest Rate Decision at Nov 03, BoE Interest Rate Decision, US Nonfarm Productivity quarterly report at Nov 04 and US Nonfarm Payrolls at Nov 05.

GBP/USD Weekly outlook:

Technical View:

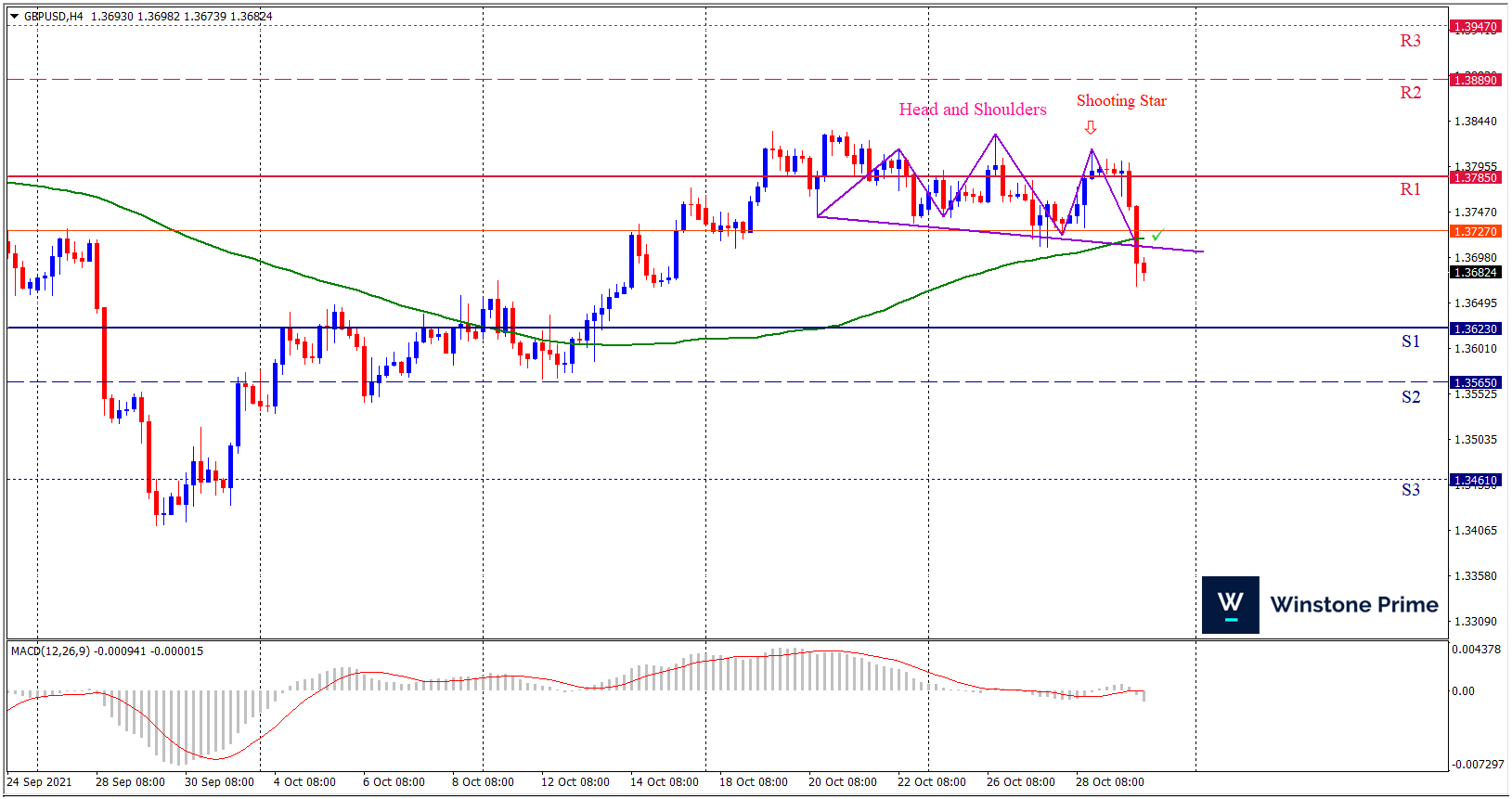

Last week’s high was 0.03% lower than the previous week. Maintaining high at 1.3830 and low at 1.3668 showed a movement of 162 pips.

In the upcoming week we expect GBP/USD to show a bearish trend. The currency pair is trading below the 100 Simple Moving Average and the MACD trades to the downside. A firm breakout below 1.3623 may fall to 1.3565 and may take a way down to 1.3461. Should 1.3785 prove to be unreliable resistance, the GBPUSD may raise upwards 1.3889 and 1.3947 respectively. Chart formation of head and shoulders pattern in H4 chart creates prospects of a bearish trend. Shooting star pattern formation braces expectation for a bearish trend.

| Preference |

| Sell: 1.3682 target at 1.3536 and stop loss at 1.3790 |

| Alternate Scenario |

| Buy: 1.3790 target at 1.3946 and stop loss at 1.3682 |