Fundamental view:

Euro had a bad week against its American rival. The prospects of aggressive rate hike from the Fed Policymakers and the idea that Eastern European crisis would take long to get resolved favored the greenback. The Russian invasion of Ukraine disturbed the supply chain and the commodity prices went to multi year highs and led to high inflation. Western nations keep on adding sanctions on Moscow which made the market sentiment sour.

The European Central Bank and the US Federal Reserve unveiled the minutes of their latest meetings. ECB portrayed that a large number of members believe that the current high level of inflation and its persistence needs immediate further steps toward monetary policy normalization, and said that “the three forward guidance conditions for an upward adjustment of the key ECB interest rates had either already been met or were very close to being met.” Meanwhile, FOMC Minutes were far more aggressive than anticipated. US policymakers “generally agreed” on reducing the balance sheet by $95 billion a month, which will likely begin in May. A maximum of $60 billion in Treasuries and $35 billion in mortgage-backed securities would be allowed to roll off per month. At the same time, the document hinted at upcoming 50 bps rate hikes, instead of the average 25 bps as hiked in March.

In this week, Eurozone S&P Global Services PMI on 5th April and EIA Crude Oil Stocks Change on 6th April favored the bullish trend whereas FOMC Minutes on 6th April and German Industrial production and US Initial Jobless Claims on 7th April favored bearish trend for the pair.

The major economic events deciding the movement of the pair in the next week are Eurozone ZEW Economic Sentiment Indicator, Federal Budget Balance at Apr 12, ECB Interest Rate Decision, ECB Monetary Policy Press Conference, US Retail Sales monthly report, Initial Jobless Claims, Michigan Consumer Sentiment at Apr 14 and Fed Industrial Production yearly report at Apr 15.

EUR/USD Weekly outlook:

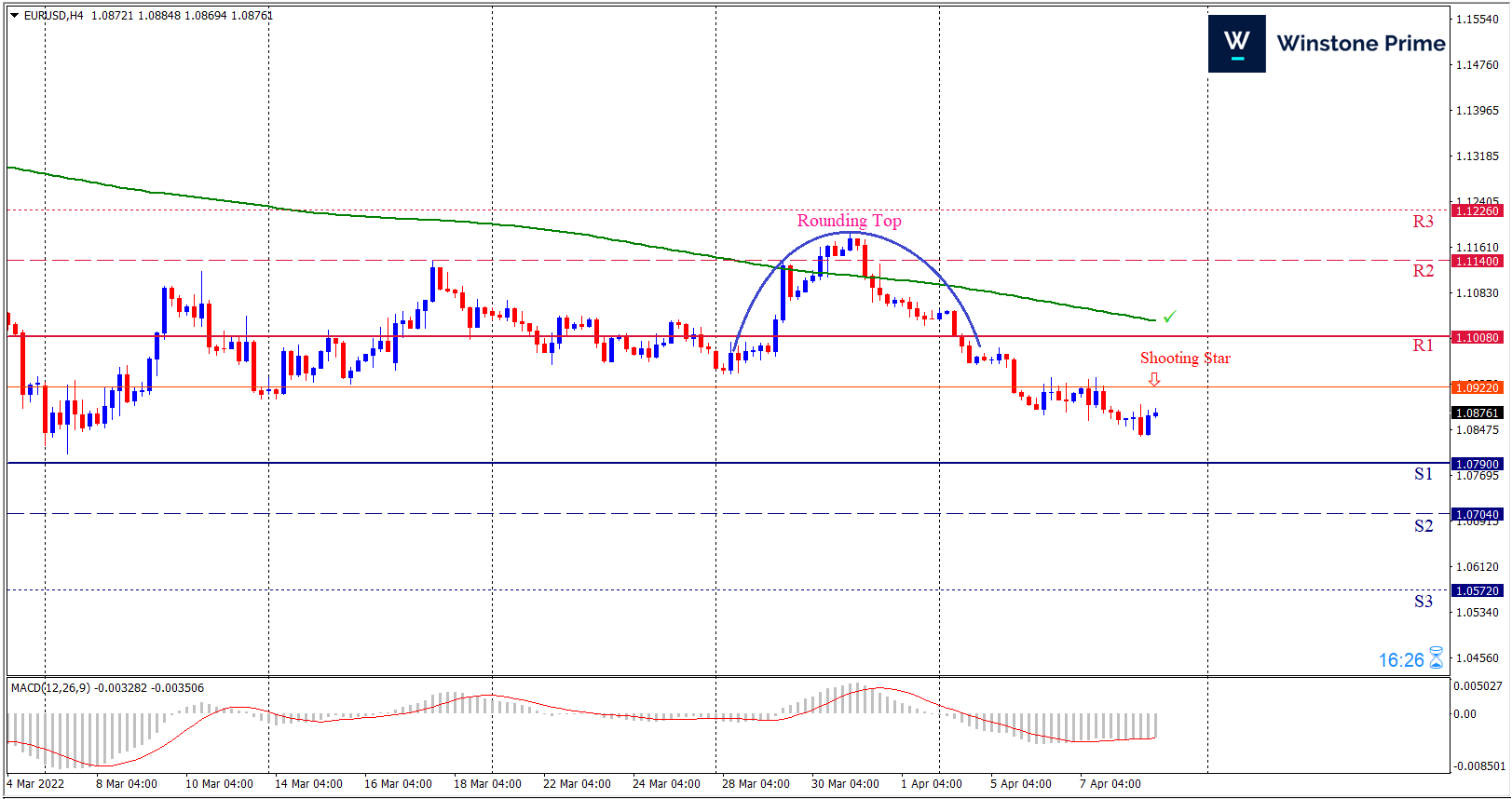

Technical View:

Last week’s high was 1.17% lower than the previous week. Maintaining high at 1.1054 and low at 1.0836 showed a movement of 218 pips.

In the upcoming week we expect EUR/USD to show a bearish trend. The currency pair is trading below the 200 Simple Moving Average and the MACD trades to the downside. Should 1.0790 proves to be unreliable support then the pair may fall further to 1.0704 and 1.0572 respectively whereas a solid breakout above 1.1008 will open a clear path upward to 1.1140 and then will further raise up to 1.1226. Chart formation of a rounding top pattern in H4 chart sets prospects for a bearish trend. Shooting star pattern formation in H4 chart escalates the expectation for a bearish trend.

| Preference |

| Sell: 1.0876 target at 1.0668 and stop loss at 1.1013 |

| Alternate Scenario |

| Buy: 1.1013 target at 1.1225 and stop loss at 1.0876 |