Fundamental view:

The Euro has gone back and forth during the course of the week again, same as it did in the previous two weeks. Market is priced at the speculation of US Federal Reserve likeliness of announcing a doubling of its bond-buying program tapering. It is expected that the Fed will double the pace of tapering to $30 billion a month. US policymakers will keep rates on hold, but pulling off support programs is the first step towards tightening, that means the chances of one or two rate hikes in 2022 have increased. On the other hand, the European Central Bank has maintained a wait-and-see stance, President Christine Lagarde says that a rate hike would be unlikely in 2022, and warns that the central bank must not rush into premature tightening.

And with the increase in cases of Omicron, European governments have announced some restrictive measures, most of them involving the use of a “green pass” to access certain places and forcing unvaccinated people to take the shots to access a more normal life.

Eurozone Industrial Production yearly report and Eurozone Trade balance on 7th December and Initial Jobless Claims on 9th December framed bearish trend Whereas ECB President Lagarde Speech on 8th December and Michigan Consumer Expectations on 10th December framed bullish trend for the pair in this week.

The major economic events deciding the movement of the pair in the next week are US Retail Sales monthly report, Fed Interest Rate Decision at Dec 15, ECB Interest Rate Decision, ECB Monetary Policy Press Conference, US Initial Jobless Claims, Fed Industrial Production monthly report at Dec 16, Eurozone Ifo Business Climate and Fed Governor Waller Speech at Dec 17.

EUR/USD Weekly outlook:

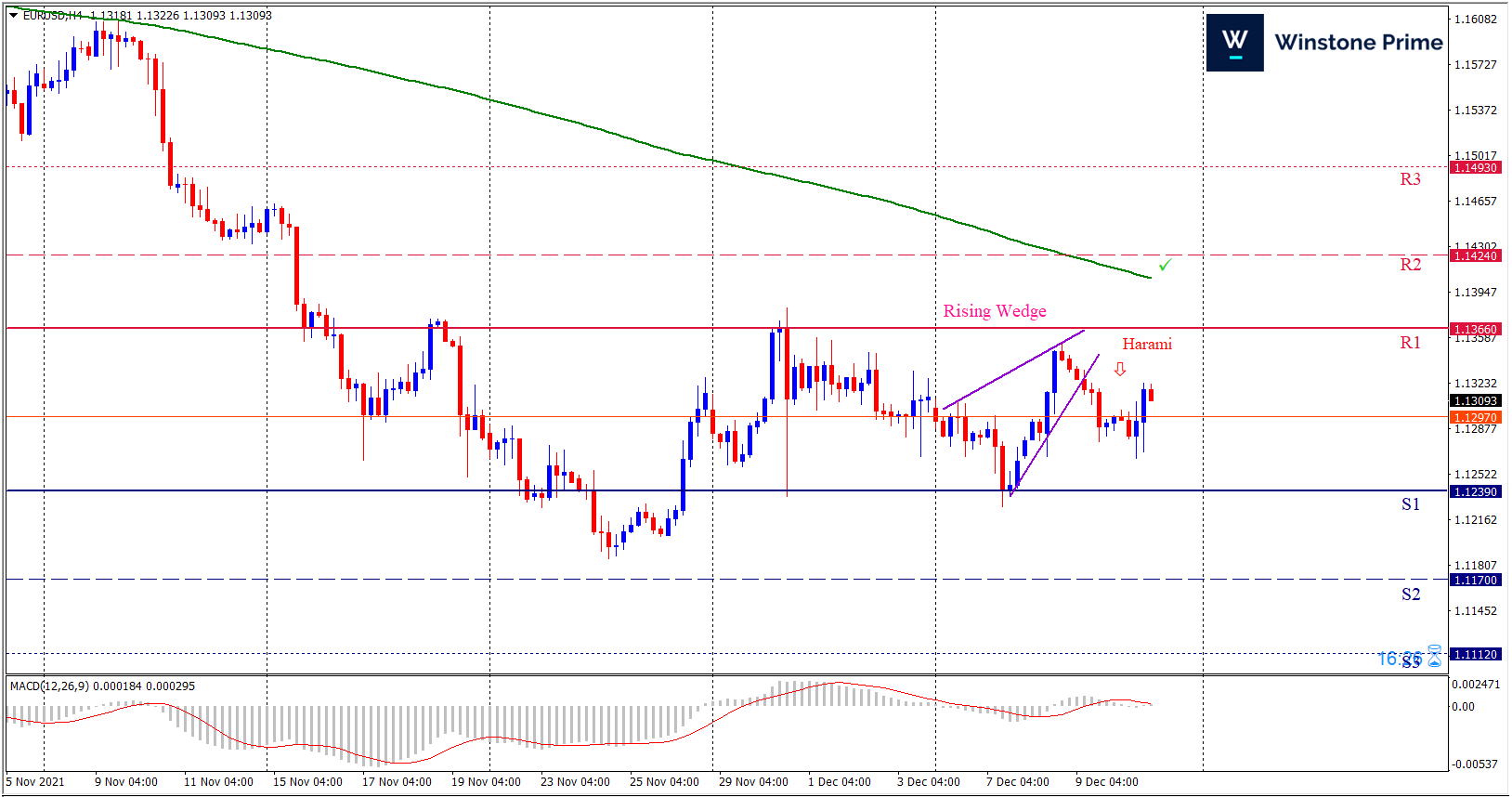

Technical View:

Last week’s high was 0.25% lower than the previous week. Maintaining high at 1.1354 and low at 1.1227 showed a movement of 127 pips.

In the upcoming week we expect EUR/USD to show a bearish trend. The currency pair is trading below the 200 Simple Moving Average and the MACD trades to the downside. Should 1.1239 proves to be unreliable support then the pair may fall further to 1.1170 and 1.1112 respectively whereas a solid breakout above 1.1366 will open a clear path upward to 1.1424 and then will further raise up to 1.1493. Chart formation of a rising wedge pattern breakout in H4 chart sets prospects for a bearish trend. Bearish harami formation in H4 chart escalates the expectation for a bearish trend.

| Preference |

| Sell: 1.1296 target at 1.1171 and stop loss at 1.1371 |

| Alternate Scenario |

| Buy: 1.1371 target at 1.1492 and stop loss at 1.1296 |