Fundamental view:

The Euro fell against the US dollar for the second consecutive week. The key catalyst for this move is the European central Bank’s (ECB) monetary policy update since President Christine Lagarde & co announced they would introduce no changes to their monetary policy. Market was expecting for a hawkish stance and rate hike from ECB whereas on contrary, ECB left rates on hold and repeated the asset purchase programs would end in Q3. Monthly net purchases will amount to €40 billion in April, €30 billion in May and €20 billion in June. President Christine Lagarde said it was “premature” to discuss quantitative tightening, adding that rate hikes could begin “sometime after” the end of the APP program.

On the other hand, US Federal Reserve officials reiterated a 50 bps rate hike in May and paved the way for a reduction of the balance sheet. This monetary policy divergence between ECB and Fed weighed on the Euro.

In this week, EIA Crude Oil Stocks Change on 13th April and US Initial Jobless Claims on 14th April underpinned the pair whereas US CPI monthly report and ZEW Economic Sentiment Indicator on 12th April and ECB Interest Rate Decision on 14th April undermined the pair- EUR/USD.

The major economic events deciding the movement of the pair in the next week are US Building Permits at Apr 19, Eurozone Industrial Production monthly report, EIA Crude Oil Stocks Change, Fed Beige Book at Apr 20, Eurozone Core CPI monthly report, US Philadelphia Fed Manufacturing Index, Initial Jobless Claims, Fed Chair Powell Speech at Apr 21 and US S&P Global Manufacturing PMI at Apr 22.

EUR/USD Weekly outlook:

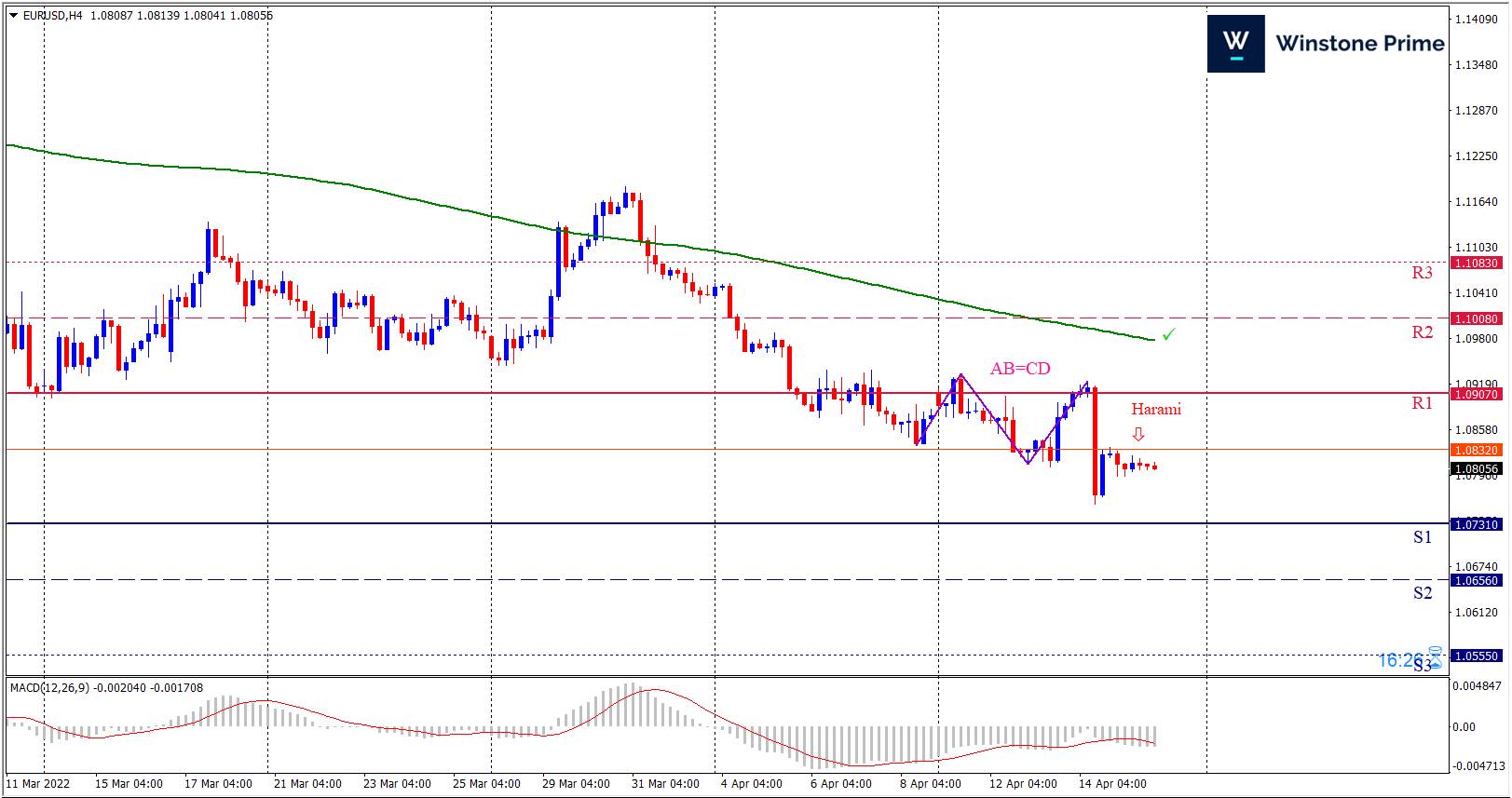

Technical View:

Last week’s high was 1.09% lower than the previous week. Maintaining high at 1.0933 and low at 1.0757 showed a movement of 176 pips.

In the upcoming week we expect EUR/USD to show a bearish trend. The currency pair is trading below the 200 Simple Moving Average and the MACD trades to the downside. Should 1.0731 proves to be unreliable support then the pair may fall further to 1.0656 and 1.0555 respectively whereas a solid breakout above 1.0907 will open a clear path upward to 1.1008 and then will further raise up to 1.1083. Chart formation of a bearish ABCD pattern in H4 chart sets prospects for a bearish trend. Bearish harami formation in H4 chart escalates the expectation for a bearish trend.

| Preference |

| Sell: 1.0805 target at 1.0657 and stop loss at 1.0912 |

| Alternate Scenario |

| Buy: 1.0912 target at 1.1082 and stop loss at 1.0805 |