The US President-elect Joe Biden unveiled a much-anticipated coronavirus rescue plan yesterday, with a promise of $2,000 in stimulus cheques to Americans, social equity, infrastructure spending, and a potential minimum wage of $15 per hour.

But, Biden did not give away the total size of the stimulus program, which, according to media reports released early Friday, is $1.9 trillion.

The Fed is currently buying US$120bn of US Treasury bonds and mortgage-backed securities every month but at some point, this spending will be tapered back. However, Powell told that now is not the time to be talking about a Fed exit.

On the employment mandate, Powell stressed the Fed’s new approach to inflation in which it will not raise rates even if unemployment falls below levels that historically would have been considered a warning sign for pricing pressures ahead.

“That wouldn’t be a reason to raise interest rates unless we start to see inflation or other imbalances that would threaten the achievement of our mandate,” he said.

“If inflation were to move up in ways that are unwelcome, we have the tools for that, and we will use them,” he said. “No one should doubt that.” “We were in a good place in February of 2020, and we think we can get back there, I would say, much sooner than we had feared,” he said.

And the rest Fed members have indicated this could occur later this year but comments from Powell indicate easing will not happen until inflation is at 2% for a year.

Apart from the latest dip in the dollar following the remarks from Powell, the dollar had risen for a second straight session, This was in line with a rise in Treasury yields, amid upbeat expectations about President-elect Joe Biden’s fiscal stimulus.

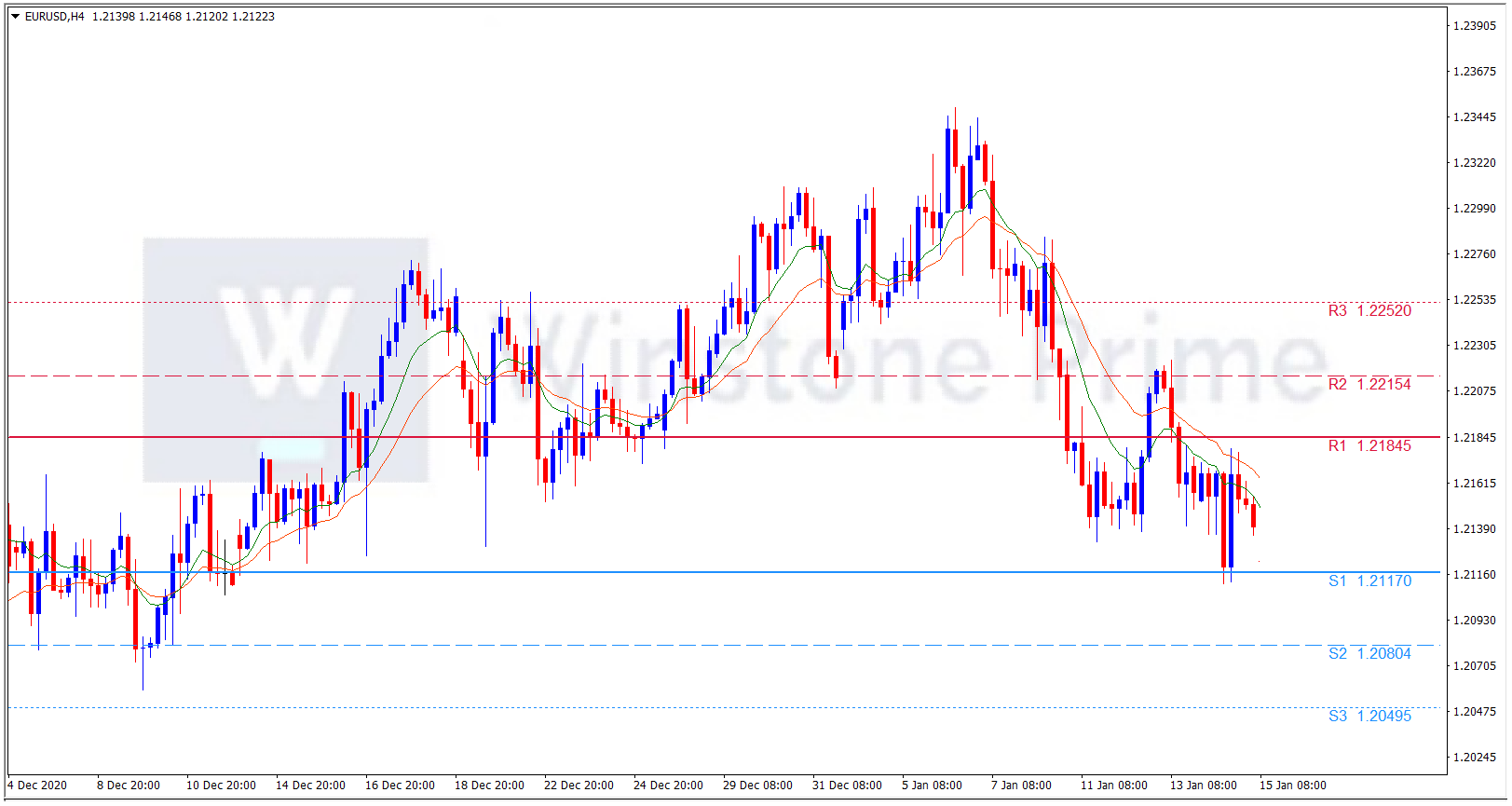

EUR/USD 4 Hour Chart:

Support: 1.2117 (S1), 1.2080 (S2), 1.2050 (S3).

Resistance: 1.2185 (R1), 1.2215 (R2), 1.2252 (R3).

Despite the fact that greenback is not favored with the powell’s speech, the dollar seems to be in uptrend against Euro and we expect a bearish trend for EUR/USD.