The coronavirus pandemic has created an economy overheating and rising inflation in the United States. Which suppress the US dollar into bearish trend and the main reason is rising in oil and gasoline prices. Rising oil and gasoline prices pushes the US economy into challenges. West Texas Intermediate, the U.S. oil-price bench mark, hit $76.98 a barrel on Tuesday, its highest level in six years, as OPEC, Russia and their allies again failed to agree on production increases.

U.S. oil companies have been cautious about investing in new exploration and production over the last year, even as oil prices have roughly doubled from the first half of 2020, when the pandemic punctured demand. The Energy Department predicts that production will average 11.1 million barrels a day this year and 11.8 million barrels a day in 2022, 400,000 barrels a day less than in 2019. Even without a surge in domestic oil production, many forecasters doubt that prices will continue to rise at their recent pace.

OPEC members generally agree that production should increase; they just disagree about how much. At the same time, the spread of new coronavirus variants has led some countries to reimpose or tighten restrictions on activity, which could dampen demand for oil. Capital Economics, a forecasting firm, said Tuesday that it expected oil prices to peak at about $80 a barrel before falling back as supply increases. But the firm said that a collapse in prices or a further spike both remained possible.

The very real risk of economic overheating by yearend can be gauged by comparing the very large size of the budget stimulus that the economy is now receiving to the estimated gap between the economy’s current level of production and that level it could attain at full employment. Heightening the chances that excessive fiscal stimulus will lead to economic overheating is the fact that the broad money supply continues to grow very rapidly while monetary policy conditions are now the easiest that they have been in more than a decade.

Further adding to demand-side inflation pressures will be the all too likely continued drawdown of the estimated $2 trillion in excess household savings that were built up during the Covid lockdown. All of this makes the Fed’s current monetary policy pronouncements very troubling. At a time that inflation appears to be accelerating and at a time that the economic overheating risk is becoming ever more likely, the Fed keeps telling us that there will be no need to raise interest rates till 2023.

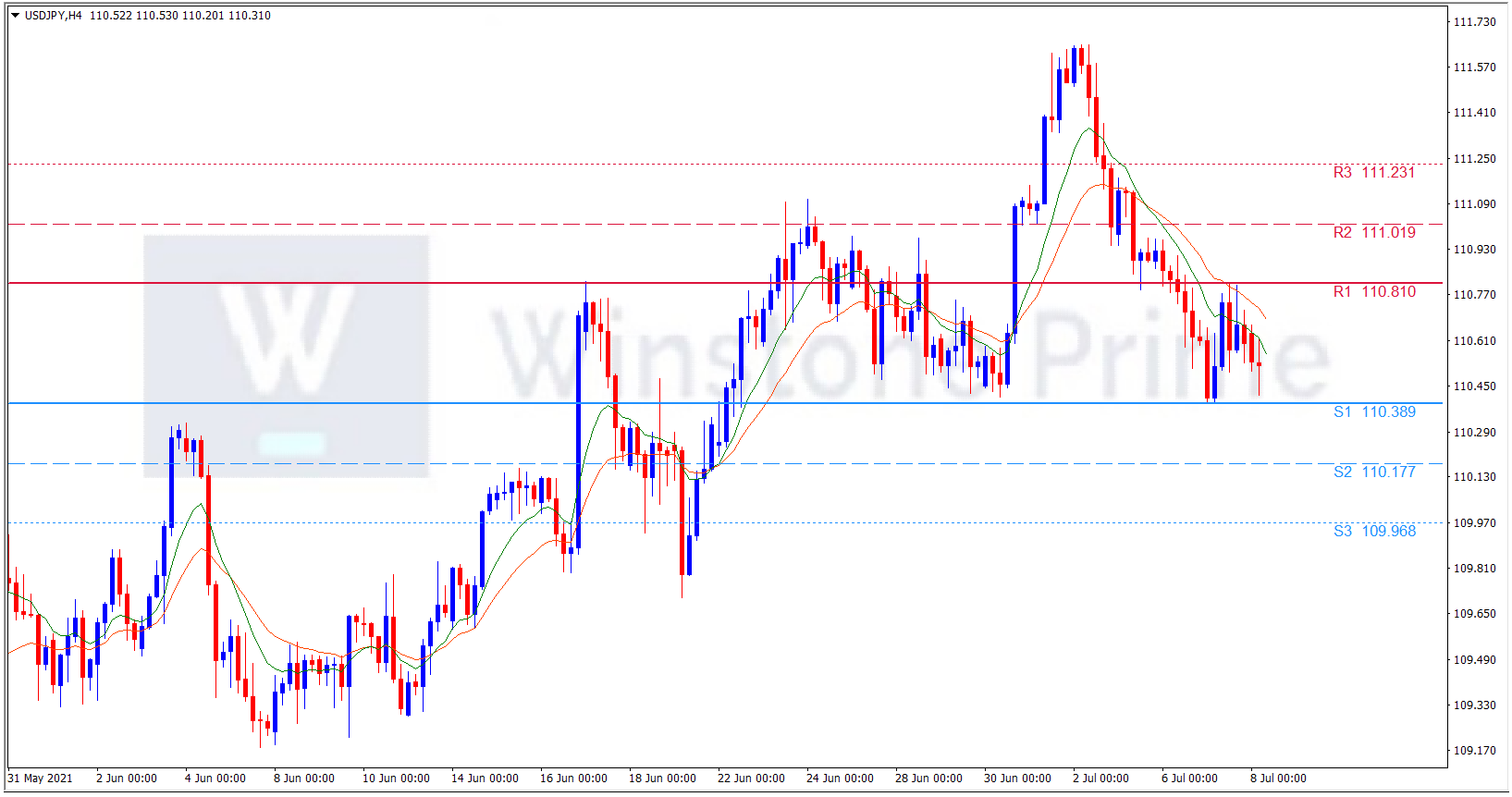

USD/JPY 4 Hour Chart:

Support: 110.39 (S1), 110.18 (S2), 109.97 (S3).

Resistance: 110.81 (R1), 111.02 (R2), 111.23 (R3).

Amidst this the rising oil prices, upward gasoline prices and rising inflation causes US into pessimistic view. We expect a bearish trend for USD/JPY.