Fundamental view:

US dollar has rallied a bit against the Japanese yen during the trading course of the week. The credit goes to the dovish Bank of Japan statement. Markets have reacted to the Fed restriction but the amount and timing of the purchase reduction is uncertain. Treasury yields in the US have spiked while Japanese Government Bond (JGB) rates have been stagnant. As expected, the Bank of Japan (BOJ) kept its ultra-loose monetary policy in place, with its main rate remaining at -0.1%, where it has been since 2016.

The policy statement noted that “Downward pressure stemming from Covid-19 is likely to remain on service, consumption, and exports and production are expected to decelerate temporarily due to supply-side constraints.”

Dallas Fed Services Business Activity on 29th October and BoJ Interest Rate Decision on 28th October framed bearish outlook whereas Japan Coincident Index on 25th October and US Core Durable Goods Orders monthly report on 27th October framed bullish outlook for the pair.

The major economic events deciding the movement of the pair in the next week are BoJ Monetary Policy Meeting Minutes, US ISM Manufacturing PMI at Nov 01, US ADP Nonfarm Employment Change, Fed Interest Rate Decision at Nov 03, Japan Markit Services PMI, US Nonfarm Productivity quarterly report at Nov 04 and US Nonfarm Payrolls at Nov 05.

USD/JPY Weekly outlook:

Technical View:

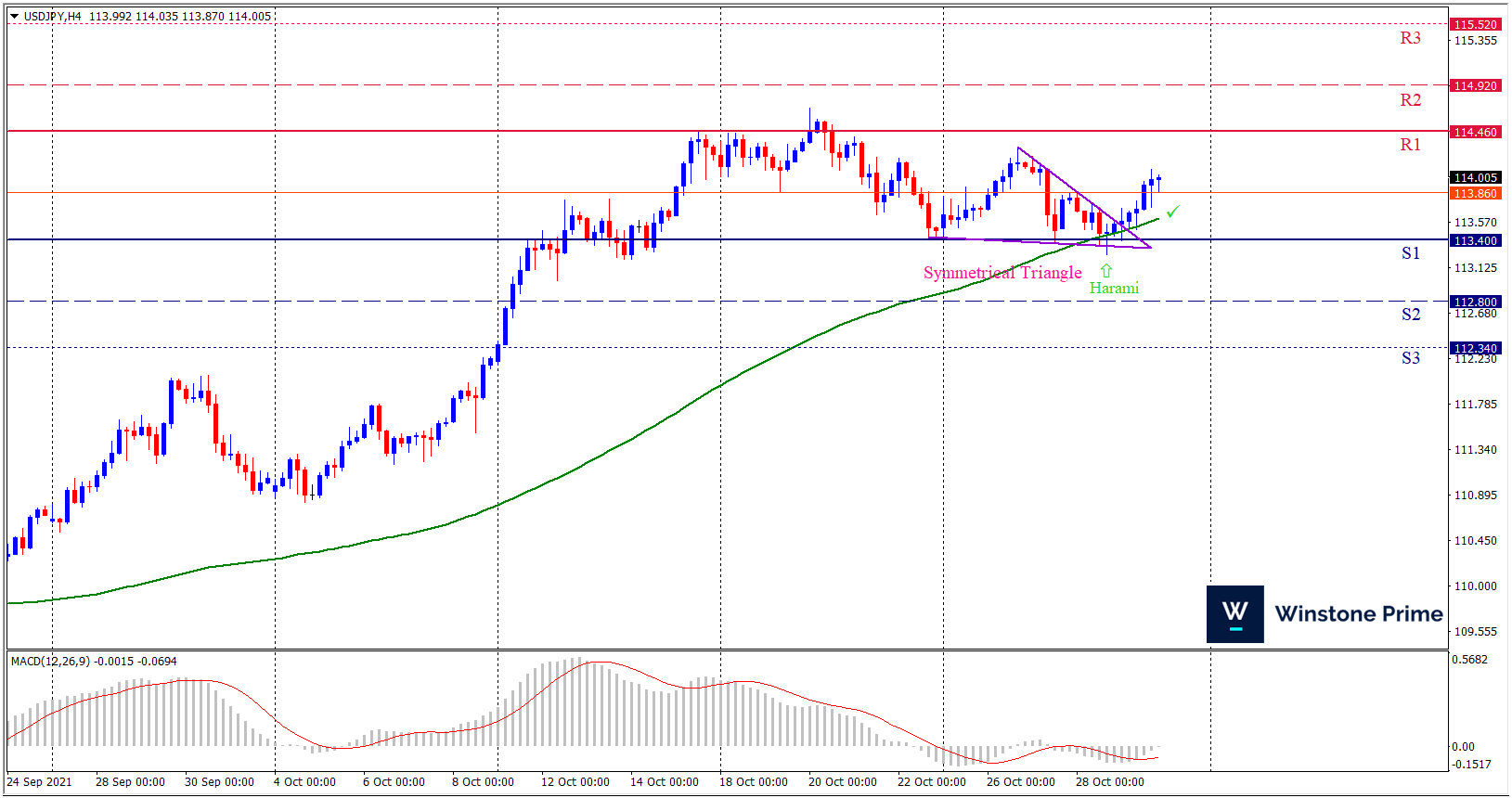

Last week’s high was 0.34% lower than the previous week. Maintaining high at 114.31 and low at 113.25 showed a movement of 106 pips.

In the upcoming week we expect USD/JPY to show a bullish trend. The currency pair is trading above the 100 Simple Moving Average and the MACD trades to the nearly neutral. A solid breakout above 114.46 may open a clean path towards 114.92 and may take a way up to 115.52. Should 113.40 prove to be unreliable support, the USDJPY may sink downwards 112.80 and 112.34 respectively. In H4 chart, Formation of symmetrical triangle breakout indicates reversal of the trend creats prospects of a bullish trend Along with a bullish harami formation braces our expectation.

| Preference |

| Buy: 114.01 target at 114.91 and stop loss at 113.35 |

| Alternate Scenario |

| Sell: 113.35 target at 112.36 and stop loss at 114.01 |