Fundamental view:

US dollar had a good start at the beginning of the week but later gave up some gains against the yen during the trading course of the week. The minutes from the Central bank’s December 16 meeting highlighted a discussion about reducing the bank’s $8.5 billion balance sheet. Fed also judged that conditions for a rate hike could be met soon suppose if the recent pace of labor market improvements continued. However, NFP was a big disappointment. December job creation registered just 199,000, less than half the 400,000 forecast.

On the other hand, Annual inflation in Tokyo was slightly stronger at 0.8% in December but the core Consumer Price Index (CPI) remained unchanged at -0.3%, which made Bank of Japan no reason to alter its ultra-accommodative monetary policy or lift its base rate from -0.1%.

US ISM Manufacturing PMI on 4th January and US Non Farm Payroll on 7th January created bearish trend whereas ADP Nonfarm Employment Change on 5th January, ISM Non-Manufacturing Employment on 6th January and Japan Household Spending yearly report on 7th January created bullish trend.

The major economic events deciding the movement of the pair in the next week are Fed Chair Powell Testimony, Japan Adjusted Current Account at Jan 11, EIA Crude Oil Stocks Change, US Federal Budget Balance at Jan 12, BoJ Corporate Goods Price Index monthly report, US Initial Jobless Claims at Jan 13, US Retail Sales monthly report and Fed Industrial Production yearly report at Jan 14.

USD/JPY Weekly outlook:

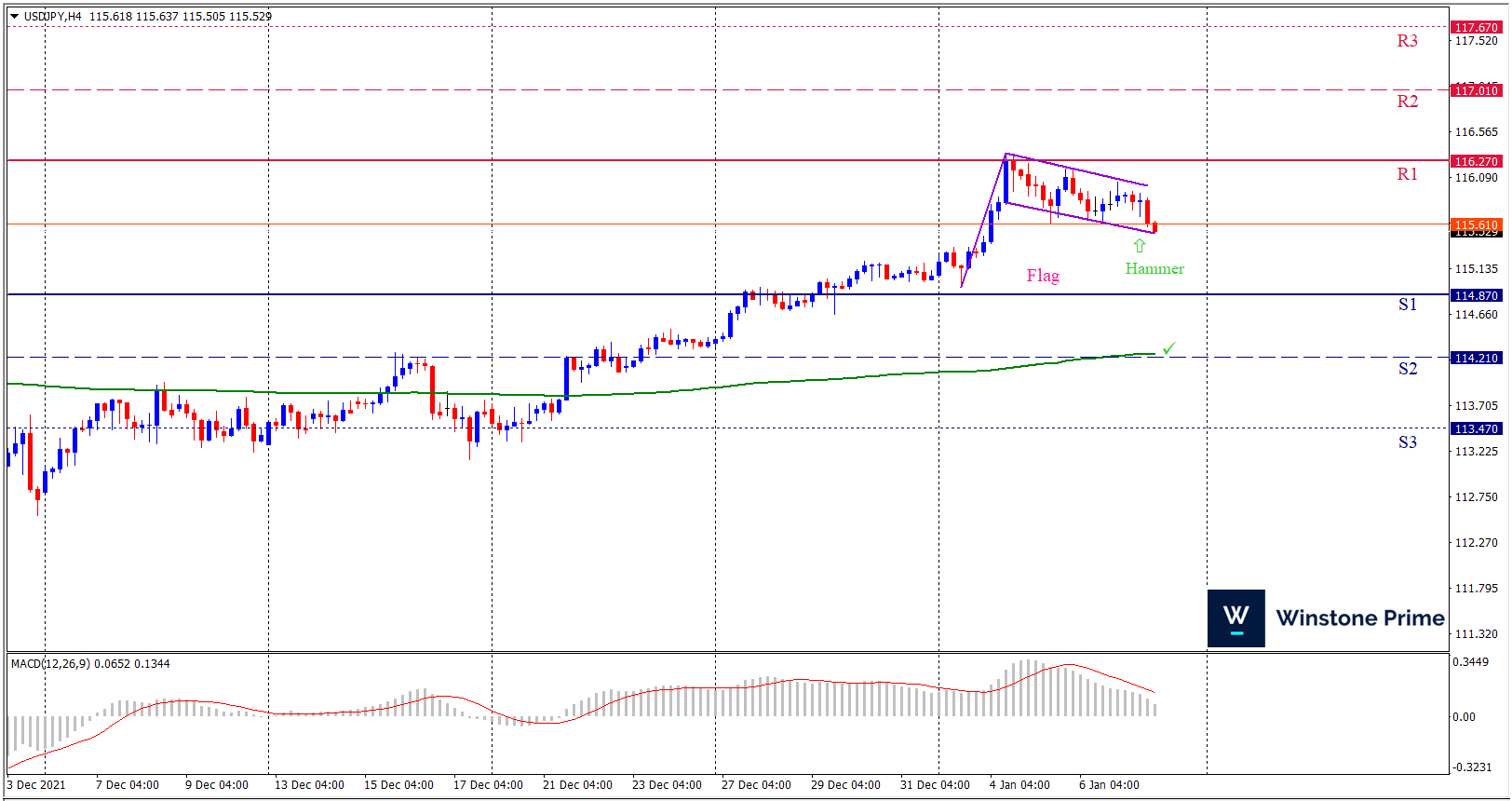

Technical View:

Last week’s high was 0.98% higher than the previous week. Maintaining high at 116.35 and low at 114.95 showed a movement of 140 pips.

In the upcoming week we expect USD/JPY to show a bullish trend. The currency pair is trading above the 200 Simple Moving Average and the MACD trades to the upside. A solid breakout above 116.27 may open a clean path towards 117.01 and may take a way up to 117.67. Should 114.87 prove to be unreliable support, the USDJPY may sink downwards 114.21 and 113.47 respectively. In H4 chart, Formation of bullish flag pattern indicates reversal of the trend creating prospects of a bullish trend Along with a hammer formation braces our expectation.

| Preference |

| Buy: 115.65 target at 117.00 and stop loss at 114.82 |

| Alternate Scenario |

| Sell: 114.82 target at 113.48 and stop loss at 115.65 |