Fundamental view:

The US dollar rallied against its yen counterpart during the trading course of the week. The aggressive stance of fed policymakers was the major catalyst favoring the dollar. The Fed unveiled the monetary policy this week. Minutes from last month’s Federal Open Market Committee (FOMC) meeting made the reduction plan concrete. “Participants generally agreed that monthly caps of about $60 billion for Treasury securities and about $35 billion for agency MBS would likely be appropriate. Participants also generally agreed that the caps could be phased in over a period of three months or modestly longer if market conditions warrant,” stated the minutes. This alongside the hawkish Fed commentary and upbeat US Services PMI data cemented a deal for a 50 bps lift-off in May which strengthened the US dollar.

On the other hand, Yen is also weighed by Japanese vulnerability to oil price fluctuations. Japan imports nearly all of its energy and GDP and her balance of payments will incur more damage from the 30% rise in Brent than the US will from the 28% increase in West Texas Intermediate (WTI). And the Japanese economic data was mixed.

In this week, ISM Non-Manufacturing PMI on 5th April and Current Account n.s.a. on 8th April favored downtrend whereas Household Spending yearly report on 5th April, FOMC Minutes on 6th April and Initial Jobless Claims on 7th April favored uptrend for the pair.

The major economic events deciding the movement of the pair in the next week are BoJ Governor Kuroda Speech at Apr 11, Federal Budget Balance at Apr 12, BoJ Governor Kuroda Speech at Apr 13, US Retail Sales monthly report, Initial Jobless Claims, Michigan Consumer Sentiment at Apr 14 and Fed Industrial Production yearly report at Apr 15.

USD/JPY Weekly outlook:

Technical View:

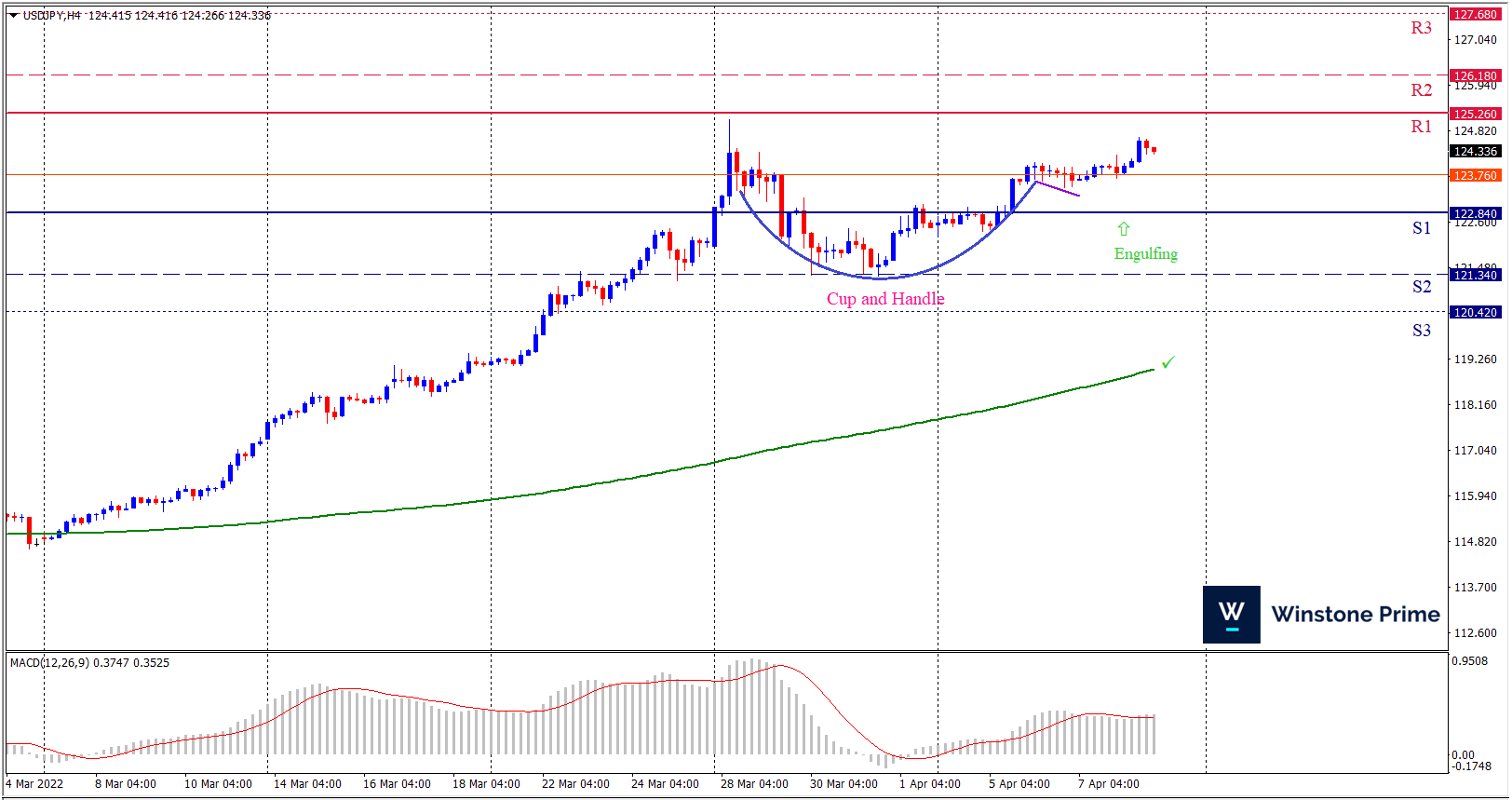

Last week’s high was 0.34% lower than the previous week. Maintaining high at 124.68 and low at 122.26 showed a movement of 242 pips.

In the upcoming week we expect USD/JPY to show a bullish trend. The currency pair is trading above the 200 Simple Moving Average and the MACD trades to the upside. A solid breakout above 125.26 may open a clean path towards 126.18 and may take a way up to 127.68. Should 122.84 prove to be unreliable support, the USDJPY may sink downwards 121.34 and 120.42 respectively. In H4 chart, Formation of cup and handle pattern indicates the trend creating prospects of a bullish trend Along with a bullish engulfing formation braces our expectation.

| Preference |

| Buy: 124.33 target at 126.49 and stop loss at 122.79 |

| Alternate Scenario |

| Sell: 122.79 target at 120.43 and stop loss at 124.33 |