Fundamental view:

The US dollar rallied against the Japanese yen during the trading course of the week. A slew of influential FOMC members, including Fed Chair Jerome Powell, left the door open for a larger rise in borrowing costs to bring down unacceptably high inflation. The markets were quick to price in the possibility of a 50 bps Fed rate hike move at the May policy meeting. The hawkish stance from Fed underpinned the USD bulls. On the other hand, Yen was undermined with BoJ’s 0.25% ceiling amid the ultra-loose policy stance adopted by the Japanese central bank.

Meanwhile, Rising metal prices in the global markets due to the Ukraine war situation are impacting the Japanese economy to a major extent. Japan which is a major importers of oil and metals is facing some serious dents in its exchange flows. Every increasing cent in the prices of commodities is widening the fiscal deficit of Japan, which eventually is hurting Japanese economics.

In this week, Japan Markit Manufacturing PMI on 24th March and US Pending Home Sales monthly report on 25th March favored downtrend whereas Fed Chair Powell Speech on 21st March, EIA Crude Oil Stocks Change on 23rd march and Tokyo CPI yearly report on 25th March favored uptrend for the pair.

The major economic events deciding the movement of the pair in the next week are Japan Unemployment Rate, US Goods Trade Balance at Mar 28, Japan Retail Sales monthly report, US CB Consumer Confidence Index at Mar 29, US ADP Nonfarm Employment Change, US GDP quarterly report at Mar 30, BoJ Tankan Large Manufacturing Index, US Initial Jobless Claims at Mar 31 and US Nonfarm Payrolls at Apr 01.

USD/JPY Weekly outlook:

Technical View:

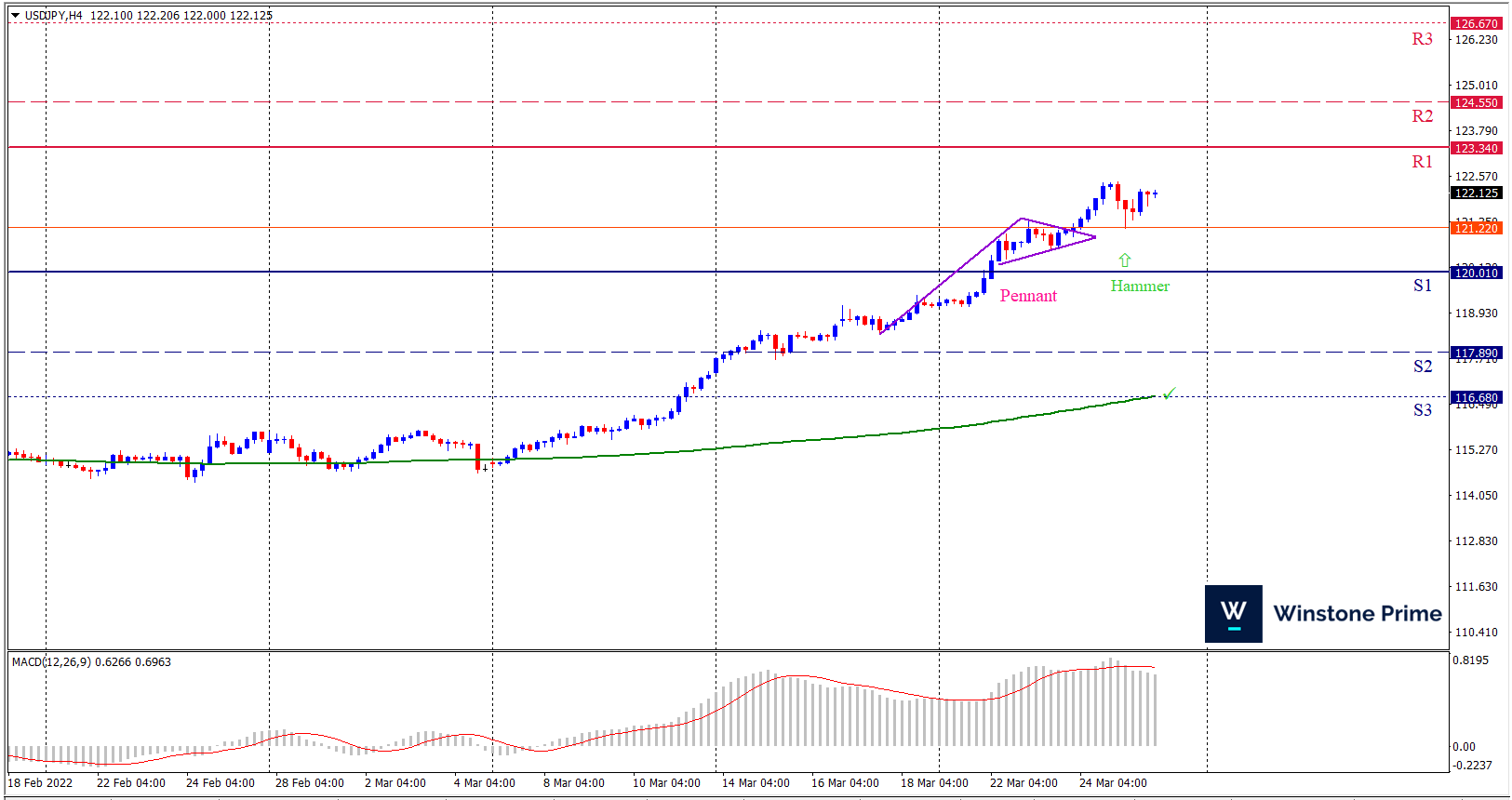

Last week’s high was 2.48% higher than the previous week. Maintaining high at 122.43 and low at 119.10 showed a movement of 333 pips.

In the upcoming week we expect USD/JPY to show a bullish trend. The currency pair is trading above the 200 Simple Moving Average and the MACD trades to the upside. A solid breakout above 123.34 may open a clean path towards 124.55 and may take a way up to 126.67. Should 120.01 prove to be unreliable support, the USDJPY may sink downwards 117.89 and 116.68 respectively. Chart formation of pennant pattern breakout upside in H4 chart favors prospects of a bullish trend Along with a hammer formation braces our expectation.

| Preference |

| Buy: 122.12 target at 124.54 and stop loss at 119.96 |

| Alternate Scenario |

| Sell: 119.96 target at 117.35 and stop loss at 122.12 |